Scam-Or Project Flash Case: Hyperliquid’s EU Access (No KYC) to MiFID II-Scope Instruments

Summary:

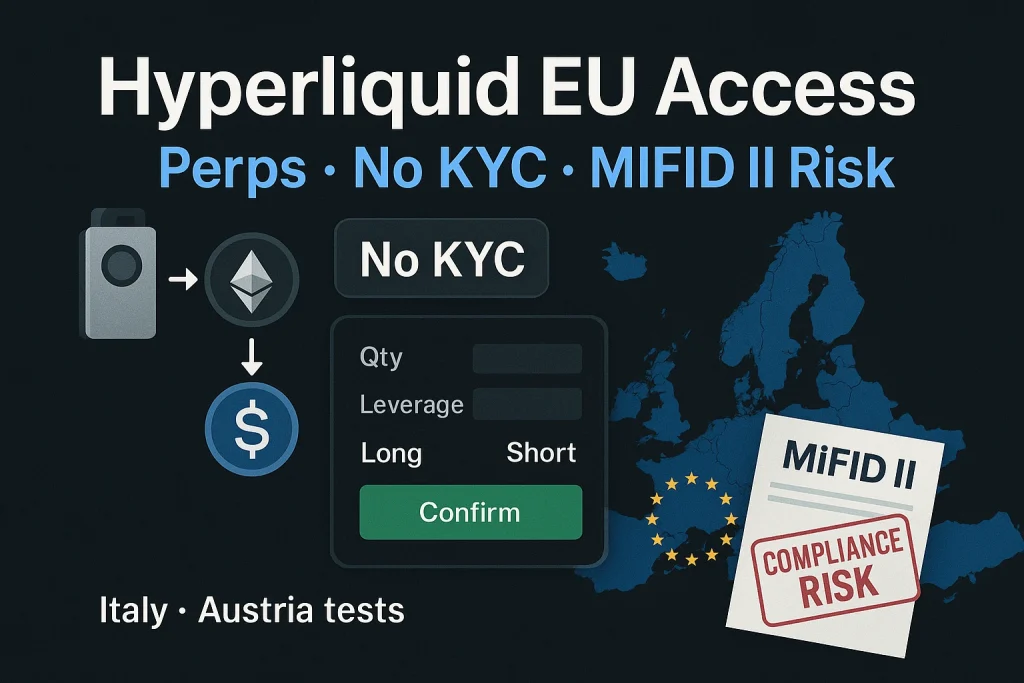

Independent checks conducted by Scam-Or Project across multiple EU locations indicate that EU residents can fund accounts, perform spot swaps, and open perpetual futures (Perps) on Hyperliquid without identity verification, geo-blocking, or explicit deposit ceilings. Testers deposited from Ledger cold wallets, converted ETH → USDC on the spot market, and opened Perps using USDC—all without KYC prompts.

Key Findings (New Evidence)

-

EU onboarding without KYC:

From several EU jurisdictions, wallets connected and the Hyperliquid UI remained fully usable with no identity checks, residency questions, or regional blocks. -

Cold-wallet funding works end-to-end:

ETH was transferred directly from Ledger to a Hyperliquid deposit address; no additional onboarding, relays, or soft caps appeared. -

Spot swap to USDC executed:

Deposited ETH was seamlessly converted to USDC on Hyperliquid’s Spot market, establishing a USDC balance. -

Perps opened with USDC:

With USDC as the trading currency, perpetual futures positions were opened and managed without KYC or gating procedures. -

No visible deposit ceilings:

Across repeated trials, no explicit deposit limits were displayed or enforced. -

Interface behavior unchanged for EU IPs:

The previously documented flow (wallet connect → ApproveAgent → accept terms) remained available from EU IP ranges.

Why This Matters (Compliance Lens)

-

Perps = derivatives:

Within the EU, perpetual futures fall under MiFID II when provided to EU clients. If a venue lets EU residents access and trade perps, investment-services authorization is ordinarily required (exchange/market-maker side). -

Anonymity heightens regulatory exposure:

Operating without KYC/appropriateness checks and without EU gating runs counter to typical MiFID II safeguards (client protection, market integrity, and AML/CFT expectations channelled through authorized firms). -

Spot ≠ clean room for perps:

Even if spot crypto-to-crypto can align with MiCA/CASP concepts, enabling EU access to perpetuals pushes the activity into the MiFID II perimeter for the provider. -

Replicated pattern across jurisdictions:

Identical results in Italy and Austria strengthen the factual basis beyond a single-country anomaly.

On-Platform Observations (Concise)

-

Deposit: ETH sent from Ledger into Hyperliquid’s deposit flow (no KYC).

-

Spot: ETH → USDC conversion completed on Hyperliquid Spot.

-

Perps: USDC used to open and manage perpetual futures positions.

-

Controls: No geo-blocking, residency selection, KYC, or deposit caps were encountered.

Quick Control Matrix (What Testers Saw)

| Control Area | Expected Under EU Norms (MiFID II context) | Observed on Hyperliquid (EU IPs) |

|---|---|---|

|

IP/Geo-fencing for Perps |

Regional gating or explicit exclusion |

Not observed |

|

KYC/Identity Verification |

Mandatory before derivatives access |

Not triggered |

|

Appropriateness/Suitability |

Assessment before enabling derivatives |

Not observed |

|

Deposit Limits |

Communicated thresholds or triggers |

None displayed |

|

Residency Attestation |

Required attestation for access |

Not requested |

Editorial Analysis (Strong View)

Hyperliquid appears to operate as a permissionless interface that, in practice, admits EU residents to derivatives trading without EU-perimeter controls. In a post-MiCA environment—where derivatives = MiFID II—this stance resembles the familiar “scale first, formalize later” approach seen in prior cycles. Jurisdictional boundaries eventually catch up with growth curves.

Updated Right-to-Reply (Questions for Hyperliquid)

-

Do you exclude EU/EEA/UK residents from Perps? If yes, where are the effective controls (IP gating, residency attestation, KYC)?

-

On what basis do you allow anonymous deposits and trading (including Ledger-funded flows) from EU IPs?

-

Why do your Terms list Restricted Persons (e.g., US/Ontario/sanctions) but omit EU/EEA/UK, while perps remain available in the UI?

-

Do you rely on reverse solicitation for EU users? If so, what evidence do you keep and how do you prevent indirect solicitation via affiliates/influencers?

-

Have you engaged any EU NCA regarding your EU access posture for perpetual futures?

Scam-Or Project will publish any response verbatim or note no comment.

Evidence Pack (On File, Timestamped)

-

How Hyperliquid addresses EU residents with crypto perps (Scam-Or Project explainer).

-

Multiple test runs: different EU jurisdictions, different IP ranges.

-

Flow artifacts: wallet-connect prompts, ApproveAgent signature, deposit confirmations, ETH→USDC spot fills, Perps order tickets/executions.

-

Hashing & timestamps: screenshots/recordings with SHA-256 hashes; environment details (IP geolocation, time, network).

-

Terms snapshot: current Terms of Use showing US/Ontario/sanctions restrictions; no EU exclusion observed.

Risk Signals for Readers

-

Regulatory: Potential unauthorized investment services risk if EU clients are admitted to perps.

-

Operational: Risk of sudden control changes (account restrictions, forced position closures, access blocks) if enforcement increases.

-

Consumer: Absence of the MiFID II investor-protection framework for these trades.

Next Steps (Scam-Or Project)

-

Transmit right-to-reply with a 72-hour response window; publish responses or note no comment.

-

Continue access monitoring via multiple EU ISPs; log any changes (geo-fencing/KYC prompts).

-

Prepare a comparative matrix (Hyperliquid vs. EU-authorized venues): KYC, onboarding, derivatives permissions, market surveillance.

-

Share information.