Perp DEX Showdown: Hyperliquid’s Reign vs. Lighter’s zk-CLOB Bet

Summary: Hyperliquid has entrenched itself as the top decentralized perpetuals venue by revenue, depth, and execution, while Lighter enters the arena with a zk-rollup CLOB, zero-fee retail, and an HLP-style liquidity vault. Is Lighter the first credible challenger—or another incentive-fueled beta sprint? (Sources: Yahoo Finanzen, The Block, Hyperliquid Docs, Lighter Docs, defillama.com, Blockchain News, Benzinga, airdrops.io, thecurrencyanalytics.com, Airdroplet.com).

Key Takeaways

-

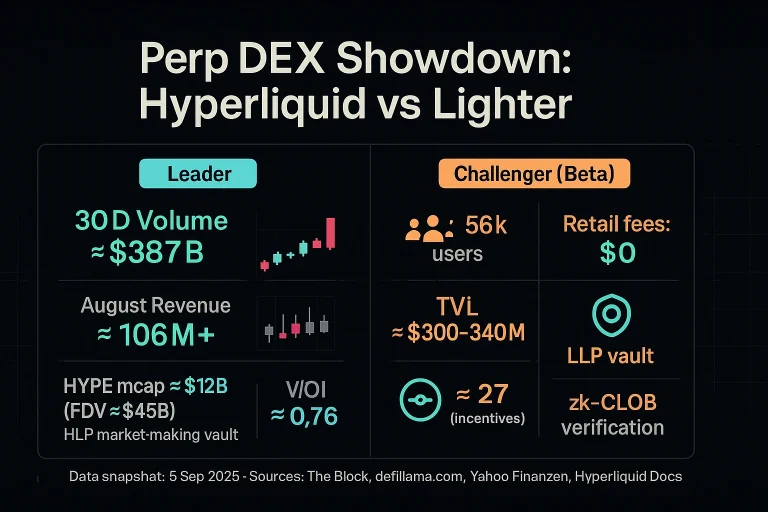

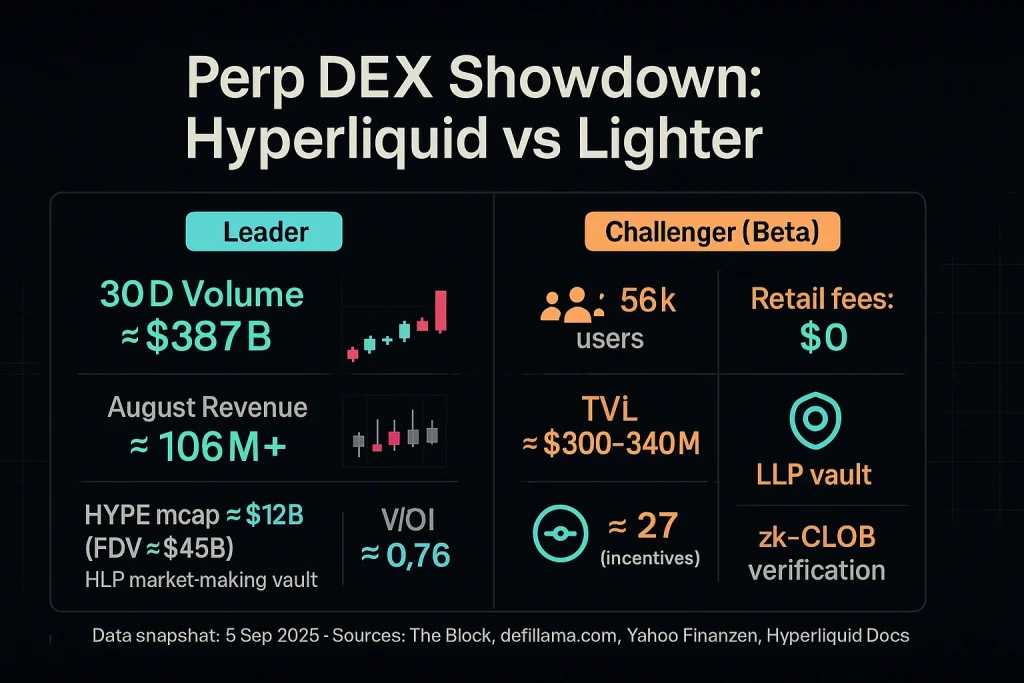

Hyperliquid is the incumbent leader: August revenue around $106–110M with ~70–80% of DeFi perps volume (methodology varies). Cumulative perp volume in the multi-trillion range.

-

HYPE + HLP flywheel: Token distribution and a community-owned HLP market-making vault power liquidity depth, uptime, and CEX-like fills.

-

Lighter’s offer: zk-rollup CLOB with verifiable matching/liquidations, zero fees for retail, and an LLP market-making vault. Public rollout just starting after closed beta.

-

Early caution flags for Lighter: ~56k users, $300–340M TVL, high volume/open-interest (V/OI) ratio indicative of incentive-amplified churn during beta.

Market Snapshot (as of 5 Sep 2025)

| Metric | Hyperliquid | Lighter |

|---|---|---|

|

30-day perp volume |

~$387B |

“Eye-catching” daily prints (beta-phase) |

|

Open interest (OI) |

~$11.9B |

OI growing, but V/OI unusually high |

|

Cumulative perp volume |

>$2.5T |

N/A (beta/new) |

|

Revenue (Aug) |

~$106M+ |

N/A (fee-free retail) |

|

Token/FDV |

HYPE ~$12B mcap (FDV ~$45B) |

Token plans pending; points live |

|

Users / TVL |

Large, entrenched |

~56k users; $300–340M TVL |

|

Status |

Mature, battle-tested |

Private beta → public rollout |

Why Hyperliquid Leads

1) Depth, Uptime, and Reliability

-

HLP vault market-makes and helps backstop liquidations.

-

Onchain governance routes fees to HLP and an assistance fund—designed to avoid opaque fee leakage.

-

Outcome: consistently tight spreads and resilience during stress events.

(Source: Medium).

2) Tokenization Loop That Stuck

-

The HYPE airdrop (late-2024/early-2025 campaigns) catalyzed growth.

-

Crucially, platform activity persisted beyond the airdrop phase—uncommon in DeFi.

3) Liquidity Flywheel at Scale

-

Better fills → more traders → deeper books → compounding network effects.

-

Data points to Hyperliquid gradually narrowing the gap with Binance derivatives share.

What Lighter Is Doing Differently

zk-CLOB Verification

-

Claims zk proofs for the full trade-execution path (not just end balances), targeting CEX-grade performance with onchain verifiability.

Retail Zero-Fee + Points

-

Fee-free retail trading and an ongoing points program; point tiers also govern how much capital users can allocate to the LLP vault.

(Source: Lighter Docs,)

LLP as Margin (Planned)

-

Post-beta, deposits in LLP may serve as trading margin, letting users earn yield while trading—a feature most perp DEXs (including Hyperliquid) don’t natively offer today.

Red Flags & Reality Checks

-

Incentive Distortion: Reported V/OI near ~27 (vs. Hyperliquid ~0.76) suggests points-driven churn. Metrics often compress once fees normalize or points end. (K33 commentary referenced.)

-

Beta ≠ Battle-Tested: Closed beta can mask slippage/latency under market stress; Hyperliquid has a track record in “extreme pile-ups.”

-

VC vs. Community: Backing from a16z/Lightspeed can accelerate shipping, but long-run durability depends on token design, unlocks, and fee routing.

Regulatory & Risk Angle (Scam-Or Project lens)

-

Perps are derivatives: Under the EU perimeter, CASP/MiCA scrutiny is tightening around leveraged crypto derivatives. Even smart-contract DEXs face pressure at on/off-ramps, especially with retail leverage and promotional incentives. Expect case-by-case enforcement through 2025–26 rather than blanket bans.

-

Market Integrity: During airdrop/points seasons, headline volumes are easily inflated. Higher-signal metrics: OI persistence, depth on non-majors, realized fees, and slippage in volatile windows.

Our Take

-

Base Case: Hyperliquid remains the default venue in the near term. The HLP model, execution reliability, and established network effects are hard moats.

-

Challenger Case: Lighter can plausibly carve out 10–20% share if it ships LLP-as-margin, maintains smart fee routing (even if not zero), and proves zk-CLOB advantages during real volatility. Expect post-incentive metric compression from beta highs.

Actionable Signals to Track (Dashboard Checklist)

Hyperliquid

-

HLP APY / net PnL trend

-

Incidents (outage/latency)

-

Per-pair depth on mid/long-tail assets

Lighter

-

Beta → public transition milestones

-

OI/volume normalization (V/OI drifting toward mature ranges)

-

LLP utilization caps tied to points program

-

Execution quality during high-vol windows

Cross-Venue

-

Share vs. Binance perps over time

-

Revenue persistence after incentives