PlatinCasino and the “Sofort” Label: How an Offshore Gambling Site Interfaces With Open-Banking Systems

PlatinCasino presents itself as an online casino operating outside the regulatory frameworks of both the United Kingdom and the European Union. Despite this offshore status, its cashier interface offers a deposit option labeled “Sofort.” Practical testing, however, indicates that this label does not reflect a classic Sofort transfer. Instead, the process relies on an open-banking authorization flow that connects users directly to regulated banking infrastructure.

This configuration effectively creates a transactional chokepoint where licensed financial rails are used to fund offshore gambling activity.

Observed Mechanics of the Deposit Process

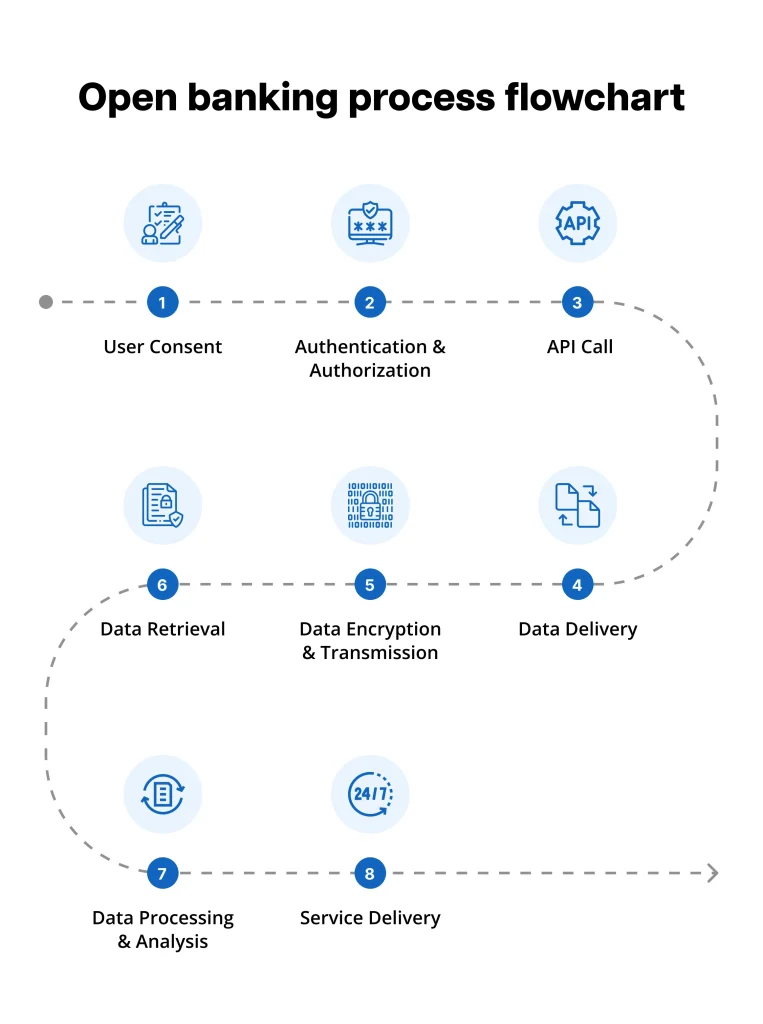

Testing of the “Sofort” option on PlatinCasino revealed a multi-step authorization path that closely resembles standard open-banking consent models rather than a direct payment method.

Key observations from the deposit flow

- Selecting “Sofort” within the PlatinCasino cashier launches an external window hosted at secure.bankgate.io, which functions as a bank selection and routing interface.

- Once a bank is chosen (for example, Revolut), the user is redirected to the bank’s official open-banking domain for authentication and consent (e.g., oba.revolut.com).

- During the authorization step, users are prompted to approve access for a third-party service provider. In documented test cases, the requesting entity appeared as PERSPECTEEV SAS.

- One of the gateway responses returned an error page carrying branding associated with SALTEDGE, suggesting a technical linkage between the bankgate.io gateway and SALTEDGE infrastructure.

- The flow allows deposits to proceed even though the casino itself operates offshore and advertises access across EU and UK jurisdictions. Details regarding the merchant of record, settlement entity, and contractual chain remain unresolved.

Transaction Path Overview (Simplified)

| Stage | Description |

|---|---|

| 1 | User initiates a deposit on platincasino.com and selects “Sofort” |

| 2 | Redirect to secure.bankgate.io for bank selection |

| 3 | Transfer to the bank’s open-banking environment (e.g., oba.revolut.com) |

| 4 | User grants consent to a named third-party provider |

| 5 | Control returns to the gateway or casino interface (final confirmation step indicated, documentation pending) |

Compliance Implications

This arrangement is not merely a matter of alternative payment branding. By leveraging open-banking authorization flows, the system introduces regulated intermediaries—such as gateways, third-party providers, and banks—into transactions that ultimately fund an offshore casino.

For end users, the “Sofort” label may imply a familiar and straightforward consumer payment method. In practice, the transaction depends on regulated banking rails, potentially redistributing compliance and risk exposure away from the gambling operator and toward financial intermediaries involved in the authorization process.

Additional Analysis

A dedicated compliance note examines the SALTEDGE-related elements of this setup in greater detail, including:

- Identified entities and their apparent roles

- Noted risk indicators within the payment flow

- Outstanding information gaps, particularly concerning merchant-of-record attribution, payee identity, and contractual relationships

The full analysis consolidates available evidence while highlighting areas where transparency remains limited.

Call for Information

Professionals with direct experience at SALTEDGE or bankgate.io, especially in roles related to onboarding, compliance, risk assessment, or partnerships, as well as users who have completed deposits through this “Sofort” pathway and can provide transaction confirmations or merchant descriptors, are invited to submit information confidentially via the Scam-Or Project whistleblower section.