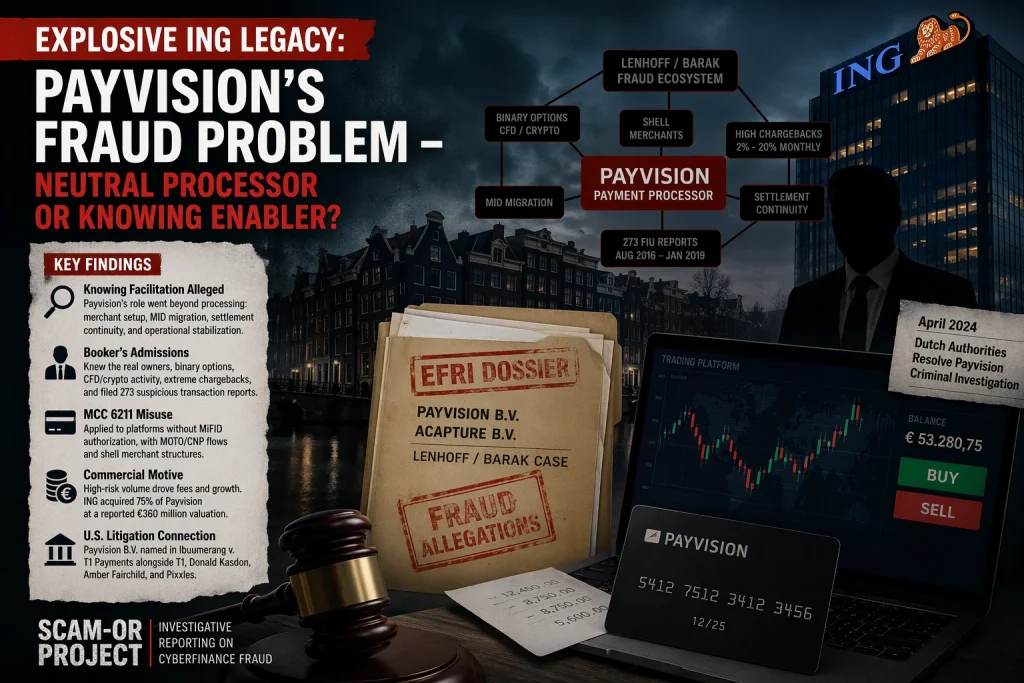

Explosive ING Legacy: Payvision’s Fraud Role — Passive Processor or Active Enabler?

At first glance, Payvision may seem like a relic from the binary options era. However, the issue is far from closed. A recently analyzed dossier suggests that Payvision was not merely a background payment processor but allegedly played a more active role in building, maintaining, and adapting the payment infrastructure that sustained the Lenhoff/Barak fraud networks.

This remains highly relevant today. Legal proceedings in Amsterdam are ongoing, and previously collected criminal evidence continues to be reassessed. In parallel, developments in the U.S., particularly around T1 Payments, indicate that similar allegations concerning European shell structures and high-risk payment processing have surfaced in litigation overseas.

Key Findings

The dossier advances a theory of “knowing facilitation”, rather than simple negligence. According to the material:

- Payvision’s role allegedly extended beyond technical processing to:

- Merchant onboarding and setup

- Migration of MIDs

- Ensuring continuity of settlements

- Stabilizing operational payment flows

- Statements attributed to Rudolf Booker play a central role. The dossier claims he acknowledged:

- Awareness of the true beneficial owners

- Familiarity with binary options, CFD, and crypto-related activities

- Exceptionally high chargeback ratios

- Submission of 273 suspicious transaction reports between August 2016 and January 2019

- The MCC classification issue is critical:

- MCC 6211 was allegedly applied to platforms lacking MiFID authorization

- MOTO and CNP flows were processed alongside shell merchant setups

- A commercial incentive is highlighted:

- High-risk transaction volumes were linked to revenue growth

- ING acquired 75% of Payvision at a reported €360 million valuation

- External context supports governance concerns:

- ING stated that the Dutch criminal investigation related to pre-acquisition activities

- Authorities in the Netherlands resolved that investigation in April 2024

- The U.S. dimension adds weight:

- Payvision B.V. appeared as a defendant in Ibuumerang v. T1 Payments, alongside T1 Payments entities, Donald Kasdon, Amber Fairchild, and Pixxles

The Payvision Dossier

There is a clear distinction between processors that overlook red flags and those that may have actively supported problematic systems. According to the dossier, Payvision falls into the latter category.

Alleged Role as Infrastructure Facilitator

The material does not portray Payvision as a passive victim of deceptive merchants. Instead, it describes the company as an integrated infrastructure partner within the Lenhoff/Barak ecosystem.

According to investigators in Germany and Austria, a large-scale fraud network involving platforms such as:

- optionstars/global

- xtraderfx

- safemarkets

- goldenmarkets

- option888

- xmarkets

- tradovest

- tradeinvest90

- zoomtrader/global

affected approximately 59,345 European consumers, generating losses of around €340 million between September 2015 and January 2019.

Within this system, Payvision B.V. and Acapture B.V. are identified as primary payment processors.

From Processor to Operational Enabler

The dossier argues that Payvision’s involvement went beyond accepting card payments and forwarding funds. It suggests participation in:

- Structuring merchant entities

- Adjusting settlement frameworks

- Maintaining continuity of payment channels

If accurate, this shifts the role from “service provider” to operational enabler.

Rudolf Booker’s Reported Knowledge

The dossier attributes several key acknowledgments to former CEO Rudolf Booker:

- Awareness that platforms were offering binary options and later CFD/crypto products

- Recognition that Lenhoff and Barak controlled multiple merchant entities

- Observed chargeback levels ranging from 2% to 20% monthly

- Filing of 273 FIU reports related to potential money laundering or terrorist financing

Such indicators typically signal high-risk exposure requiring termination of relationships. However, the dossier claims operations continued.

The MCC 6211 Classification Issue

A central compliance concern involves the use of MCC 6211, typically reserved for licensed brokerage or securities services.

According to the dossier:

| Aspect | Allegation |

|---|---|

| MCC usage | Applied to platforms without MiFID authorization |

| Transaction types | Included MOTO and CNP flows |

| Merchant structures | Utilized shell entities |

| Effect | Masked the true regulatory and risk profile |

If confirmed, this would indicate not just compliance failure, but a system that potentially reframed high-risk activity as lower-risk processing.

ING Acquisition and Commercial Context

The dossier links Payvision’s high-risk volumes to financial incentives. In early 2018, ING acquired a 75% stake in Payvision at an estimated €360 million valuation.

The argument presented:

- Increased transaction volume → higher fees

- Revenue growth → improved valuation metrics

While this does not prove intent, the commercial rationale is considered plausible.

The U.S. and T1 Payments Connection

The dossier notes that similar allegations appeared in U.S. cases between 2019 and 2022. These included claims that Payvision assisted merchants in establishing European corporate structures to gain access to card processing.

Public Nevada court records confirm that:

-

Payvision B.V. was named in

Ibuumerang, LLC v. T1 Payments LLC et al. - Other defendants included:

- T1 Payments LLC

- T1 Payments Limited

- TGlobal Services Limited

- Donald Kasdon

- Amber Fairchild

- Pixxles, Ltd.

Although settlement details remain unclear, the case demonstrates that Payvision was directly involved in U.S. litigation connected to the T1 ecosystem.

Editorial View (Scam-Or Project)

The central takeaway is straightforward.

This is not a narrative about a processor that simply reacted too slowly. The dossier portrays Payvision as an entity that allegedly contributed to building and maintaining the financial infrastructure behind fraudulent operations — despite multiple warning signals.

If this interpretation holds, Payvision’s role was not incidental. It was structural.

That is precisely why the case has regained attention.

Whistleblower Call

Scam-Or Project invites insiders, former Payvision employees, merchants, compliance specialists, and affected users with relevant information regarding Payvision, Rudolf Booker, ING, T1 Payments, or related structures to submit reports via the Scam-Or Project whistleblower section.

Confidential disclosures remain essential for uncovering how payment systems are used in cyberfinance fraud.