Capitolio’s Legal Threat Reinforces the Rail Atlas Thesis: Open-Banking Payees, Casino-Origin Funds, and Payment-Purpose Dilution

Editorial Note: The legal notice referenced in this article was signed by an individual identifying himself as Hennadii Postnov, Director of Capitolio Inc. Scam-Or Project has not yet independently verified this claimed director status through publicly available corporate records. Capitolio is invited to provide an Alberta corporate registry extract, board resolution, or other documentation confirming Mr. Postnov’s authority to represent the company.

After Scam-Or Project identified CAPITOLIO INC. as the visible payee within a tested 1Go Casino Revolut/Yapily open-banking deposit route, the Canadian MSB issued a legal demand requesting removal of the report. However, the notice itself does not appear to dispute the central payment-rail observation. Instead, Capitolio effectively acknowledges that its entity may appear as the named payee in transactions routed through its open-banking on-ramp infrastructure.

Following publication, two notable developments occurred:

- Capitolio appears to have revised regulatory information displayed on its website;

- 1Go Casino appears to have removed the Revolut funding option from its cashier.

These developments further support the core Rail Atlas methodology: public scrutiny of payment infrastructure can trigger rapid operational adjustments.

Two-Minute Briefing

The Scam-Or Project Rail Atlas initiative was designed to map how offshore casino deposits travel through:

- payment gateways,

- open-banking providers,

- wallet infrastructure,

- crypto payment rails,

- regulated processors,

- and bank-facing authorisation layers.

The 1Go Casino / Capitolio case has become a particularly clear example of this methodology in action.

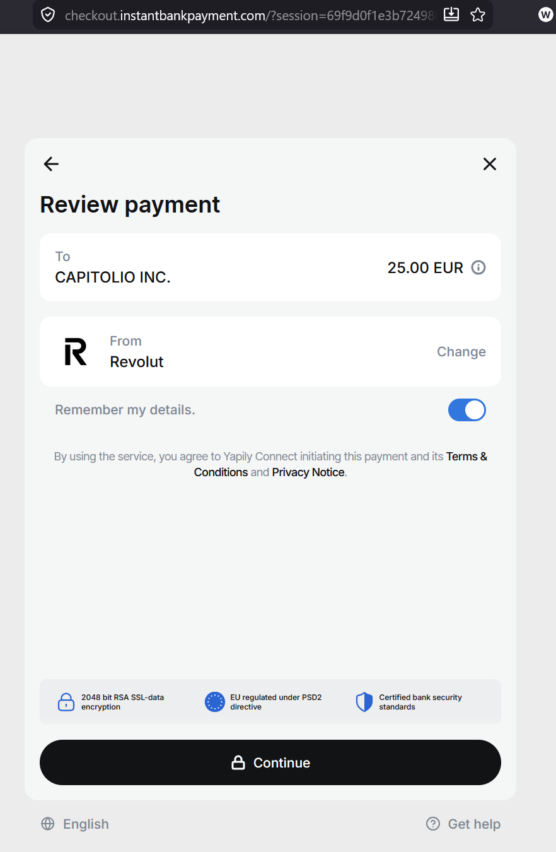

In the original review, a tested deposit flow from the 1Go Casino cashier passed through multiple intermediary routing layers before ultimately reaching a Revolut/Yapily open-banking authorisation screen displaying CAPITOLIO INC. as the visible payee.

Capitolio later sent a formal legal notice demanding complete removal of the article. The company alleged defamation and misleading reporting. However, the notice does not appear to directly challenge the screenshot-based evidence showing Capitolio as payee. Instead, Capitolio states that appearing as payee is part of the standard architecture of its open-banking on-ramp infrastructure.

That clarification is highly significant.

The core issue is no longer whether Capitolio appeared as payee — Capitolio’s own position appears to confirm that possibility. The real compliance question becomes:

When a user initiates a deposit from an offshore casino cashier, do banks, PISPs, MSBs, and transaction-monitoring systems still see the underlying gambling context if the bank-facing payee is a payment infrastructure entity rather than the casino brand itself?

If not, the structure may create what Scam-Or Project describes as payment-purpose dilution.

Key Findings

| Issue | Observation |

|---|---|

| Legal notice | Capitolio demanded removal of the article but did not clearly dispute the central rail evidence |

| Payee confirmation | Capitolio acknowledged that it may appear as named payee within its open-banking infrastructure |

| Methodological impact | The case strengthens the Rail Atlas concern regarding non-casino payees in casino-origin transactions |

| Editorial adjustments | Scam-Or Project removed “Illegal Payment Services,” removed a personal name, and replaced “scheme” with “operating model” |

| Website modification | Capitolio appears to have updated regulatory information displayed on its public pages |

| Revolut rail | The Revolut funding route appears to have been removed from the 1Go Casino cashier |

| Alternative rails | Other Pay by Bank and open-banking rails remain active |

| Updated routing | New flows appear linked to Bridge / SaltEdge infrastructure |

| Visible payees | Domus Payment Solutions still appeared as payee in another Pay by Bank route |

What Capitolio’s Notice Actually Confirms

Capitolio’s legal notice relies on arguments involving:

- Alberta defamation law,

- Austrian legal provisions,

- GDPR-related concerns,

- and EU platform rules.

However, from a payment-infrastructure perspective, the most important element of the notice is this:

Capitolio states that it appears as named payee in transactions processed through its Open Banking on-ramp infrastructure.

Capitolio presents this as a standard technical arrangement. Scam-Or Project’s interpretation differs.

If an infrastructure provider consistently appears as the bank-facing payee in transactions originating from casino cashiers, then several compliance questions emerge:

- Does the bank still see the upstream merchant?

- Is the gambling context preserved?

- Is the payment classified correctly?

- Can monitoring systems detect casino-origin funds?

- Does the customer understand who ultimately receives the payment?

This is the core Rail Atlas concern.

Capitolio’s Position vs. Scam-Or Project’s Interpretation

| Issue | Capitolio’s Position | Scam-Or Project’s Interpretation |

|---|---|---|

| Payee appearance | Capitolio states it appears as named payee within its infrastructure | This confirms the observed payee role |

| Technical architecture | Capitolio argues the setup is standard | Standard infrastructure can still create compliance blind spots |

| 1Go Casino flow | Capitolio disputes the framing | The tested flow still showed CAPITOLIO INC. as payee |

| “Scheme” wording | Capitolio objected | Replaced with “operating model” |

| Categories | Capitolio objected to “Illegal Payment Services” | Scam-Or Project adjusted editorial framing |

| Personal-data concerns | Capitolio objected to a compliance officer’s name | The name was removed |

| Core issue | Capitolio says no violation is proven | Scam-Or Project argues the structure raises legitimate AML/compliance concerns |

Why the Capitolio Case Matters

The Capitolio response illustrates a recurring pattern in modern payment-rail investigations.

Infrastructure providers often do not deny the underlying architecture. Instead, they argue:

- the structure is standard,

- technically necessary,

- or common within open-banking environments.

However, “standard architecture” does not automatically eliminate systemic compliance risk.

If the consumer-facing merchant differs from the bank-facing payee, regulators and compliance teams must ask:

- Who is the actual merchant?

- Who onboarded the merchant?

- Who knows the payment originated from a casino?

- What information reaches the bank?

- What information reaches the PISP?

- How is the transaction categorised?

- Are gambling restrictions being bypassed indirectly?

The answer cannot simply be:

“This is how open banking works.”

If the architecture removes the casino brand before the transaction reaches the bank-facing layer, then the model may create a monitoring blind spot.

The CSSF / RCS Issue and the Website Changes

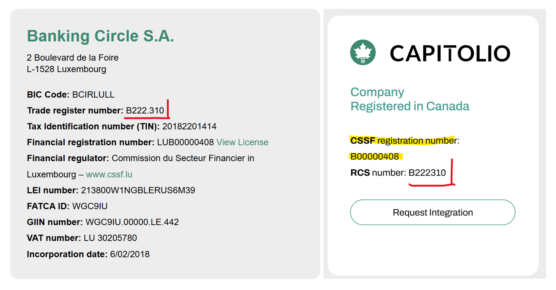

One of the original findings concerned unusual regulatory information previously displayed on Capitolio’s website.

Earlier screenshots reportedly showed:

| Displayed Information |

|---|

| Company Registered in Canada |

| CSSF registration number: B00000408 |

| RCS number: B222310 |

These identifiers correspond to Luxembourg-style regulatory references associated with Banking Circle S.A., whose official website lists:

- financial registration number LUB00000408,

- trade register number B222.310,

- CSSF registration number B00000408.

Scam-Or Project did not claim that Capitolio was connected to Banking Circle. The concern related to regulatory representation and website integrity.

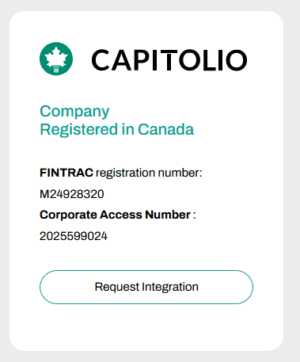

Following publication, Capitolio appears to have revised the displayed information. Current pages reportedly show:

- FINTRAC registration number M24928320,

- Alberta Corporate Access Number 2025599024.

This represents a concrete compliance-reporting outcome: a publicly visible regulatory-information anomaly appears to have been corrected after exposure.

Updated 1Go Casino Cashier Review

A subsequent review of the 1Go Casino cashier suggests the Revolut funding route has disappeared.

The updated cashier still displayed:

- Crypto Currency,

- ByBit,

- Pay by Bank,

- additional account-to-account payment rails.

This suggests that the original Revolut/Yapily route may have been disabled or replaced following publication.

However, the broader infrastructure issue remains unresolved.

The updated review reportedly identified:

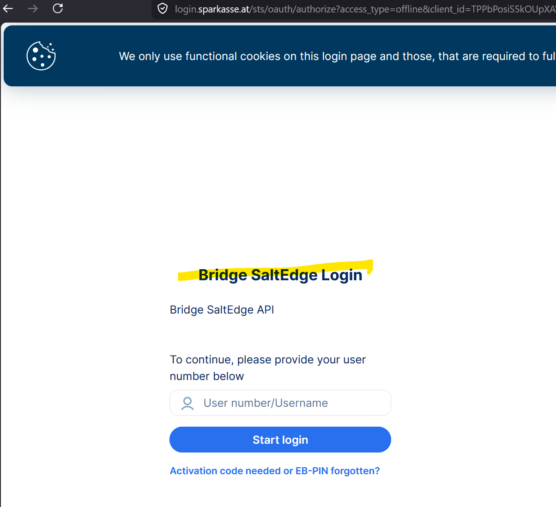

- Domus Payment Solutions as payee within another Pay by Bank route;

- routing through secure.bankgate.io;

- bank authentication pages referencing Bridge SaltEdge API.

Both Bridge and Salt Edge publicly market open-banking and payment-initiation services.

Updated 1Go Rail Map

Original Revolut / Yapily / Capitolio Route

| Layer | Observed Element | Compliance Relevance |

|---|---|---|

| Casino cashier | 1Go Casino | Deposit originates from offshore casino |

| Gateway layer | BillBlend | Initial routing layer |

| Gateway layer | SegoPay | Additional intermediary |

| Gateway layer | Tryzto | Opaque routing layer |

| Open-banking bridge | InstantBankPayment | Transition into banking flow |

| Regulated PISP | Yapily Connect UAB | Open-banking authorisation layer |

| Bank-facing interface | Revolut OBA | Final authorisation screen |

| Visible payee | CAPITOLIO INC. | Non-casino payee shown to bank |

Updated Pay by Bank / Bridge / SaltEdge Route

| Layer | Observed Element | Compliance Relevance |

|---|---|---|

| Casino cashier | 1Go Casino | Deposit still begins within casino environment |

| Payment method | Pay by Bank | Account-to-account funding remains active |

| Routing domains | secure.bankgate.io / checkout.instantbankpayment.com | Gateway layer |

| Open-banking interface | Bridge SaltEdge API | Alternative open-banking infrastructure |

| Facilitators |

Bridge by Perspecteev / Salt Edge (https://bridgeapi.io) / (https://saltedge.com) |

Regulated open-banking providers |

| Authentication layer | Bank login screen | User authorisation stage |

| Visible payee | Domus Payment Solutions | Non-casino payee remains visible |

Rail Atlas Methodology: Why This Case Matters

The Capitolio case demonstrates why Scam-Or Project maps complete payment rails instead of merely listing payment options.

A casino cashier screenshot is only the starting point.

The real questions emerge later:

- Which gateway appears?

- Which intermediary domains are used?

- Which PISP becomes involved?

- Which bank-facing authorisation screen appears?

- Who is shown as payee?

- Does the gambling context remain visible?

- Do the rails change after public exposure?

Capitolio’s own notice appears to answer one of those questions directly:

Capitolio may appear as named payee in open-banking on-ramp transactions.

That may be technically accurate.

But if the transaction originated from an offshore casino cashier, the compliance implications remain highly relevant.

Why This Matters for Payment Processors

Scam-Or Project’s reporting focuses on visibility and accountability across high-risk payment rails.

The objective is not opposition to open banking or financial innovation.

The concern is whether regulated or semi-regulated infrastructure is being used to facilitate offshore casinos operating in jurisdictions where they may lack local authorisation.

1Go Casino publicly references:

- Galaktika N.V. as operator,

- Curaçao licence OGL/2024/169/0146,

- Unionstar Limited as payment agent.

A Curaçao licence does not automatically permit unrestricted operation across EU jurisdictions.

That is where payment processors, PISPs, MSBs, and banks become relevant.

The key expectation is straightforward:

Payment architecture should not transform a casino-origin transaction into an ordinary-looking transfer to a payment infrastructure entity.

Regulatory Questions Raised

The Capitolio response and updated 1Go flows raise several unresolved questions:

- If an open-banking provider appears as payee, how is the underlying merchant disclosed?

- Who classifies the transaction as gambling-related?

- Can banks detect casino-origin funds if the payee is an MSB or PSP?

- Do PISPs receive upstream merchant-category information?

- Must processors block casinos targeting unauthorised jurisdictions?

- When one rail disappears after exposure, is the merchant terminated or simply rerouted?

- Does replacing one rail with another represent remediation or rotation?

- Should open-banking consent screens disclose the underlying merchant rather than only the technical payee?

These questions are no longer theoretical. They are visible in live payment flows.

Conclusion

Capitolio’s legal notice did not weaken the Rail Atlas methodology. It reinforced it.

The central finding remained unchanged:

A tested 1Go Casino Revolut/Yapily deposit flow displayed CAPITOLIO INC. as the visible payee.

Capitolio’s response did not clearly dispute that observation. Instead, it explained that such payee appearances are part of its infrastructure model.

That is precisely why the case matters.

If the casino brand disappears before the payment reaches the bank-facing layer, then payment-purpose dilution may occur.

The aftermath is equally revealing:

- Capitolio appears to have revised website regulatory information;

- the Revolut rail appears removed;

- other Pay by Bank routes remain active;

- Domus Payment Solutions still appeared as payee;

- Bridge/SaltEdge infrastructure now appears within updated flows.

The rail changes.

The payee changes.

The gateway changes.

The compliance question remains.

Scam-Or Project will continue mapping payment rails and examining how offshore casino deposits move through regulated financial infrastructure.

The essential question remains:

Do banks, processors, PISPs, and monitoring systems know when an ordinary-looking account-to-account payment actually originated from an offshore casino deposit?

Call for Information

If you have information regarding Capitolio or other payment facilitators linked to offshore casino infrastructure, you may submit documentation, screenshots, or payment records through the Scam-Or Project Complaints section. Relevant whistleblower materials may assist ongoing payment-rail investigations.