Passpoint Under Scrutiny After Appearing as Payee in Betify’s EU Casino Payment Rail

African Payment Orchestration Platform Linked to Offshore Casino Deposit Flow

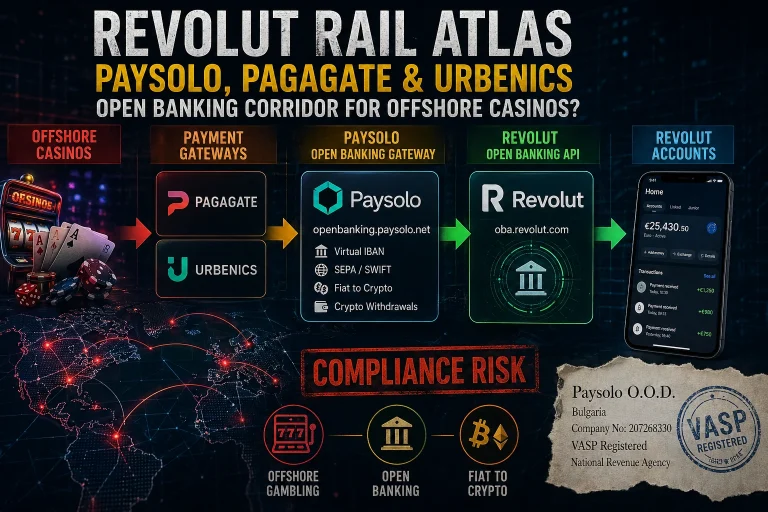

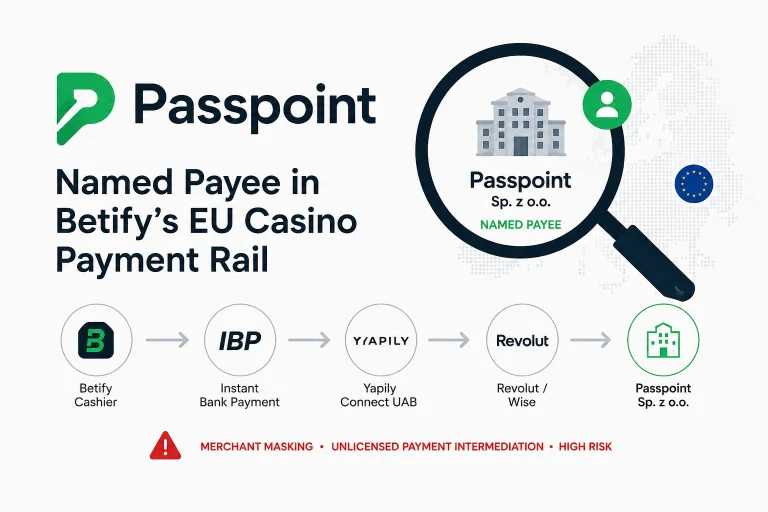

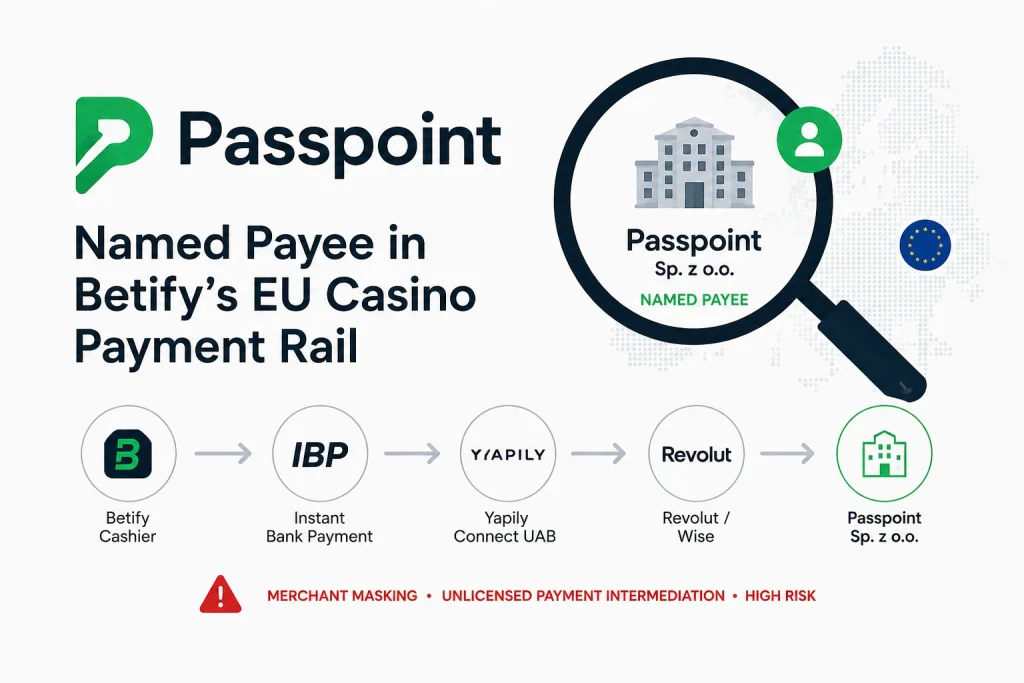

Passpoint presents itself as a financial orchestration platform connecting businesses with payment, FX, compliance, liquidity, and settlement infrastructure across Africa, Europe, and G20 markets. However, a May 2026 investigation by Scam-Or Project uncovered a far more controversial role for the company. During a review of Betify’s payment infrastructure, Passpoint Sp. z o.o., the Polish entity linked to the Passpoint group, surfaced as the named payee within an EU-facing open-banking casino payment flow.

This was not merely a technical routing trace. In open-banking and account-to-account transfers, the payee is the visible recipient presented to the payer and banking infrastructure. Unless Passpoint can demonstrate a clear regulatory and contractual framework for this role, the structure raises serious concerns regarding merchant masking, unlicensed payment intermediation, and potential transaction-laundering exposure.

Executive Summary

Passpoint operates through the domain mypasspoint.com and describes itself as a financial orchestration layer serving Africa, Europe, and G20 payment corridors. The company publicly states that it is “not a payments company,” but rather a platform connecting businesses to global financial infrastructure through a unified API supporting pay-ins, payouts, FX, liquidity, compliance, and settlement services.

That narrative now faces scrutiny following findings from Scam-Or Project’s May 2026 Betify review. The investigated bank-transfer and open-banking deposit route was structured as follows:

Observed Betify Payment Flow

| Step | Entity |

|---|---|

| 1 | Betify Cashier |

| 2 | InstantBankPayment |

| 3 | Yapily Connect UAB |

| 4 | Revolut / Wise |

| 5 | Passpoint Sp. z o.o. |

The key issue is straightforward: Passpoint Sp. z o.o. appeared as the payee in the transaction chain.

In open-banking infrastructure, the payee is not a background API provider or invisible processor. The payee is the payment-facing recipient shown to both the customer and financial institutions involved in the transfer. This places Passpoint directly in the operational and compliance layer of the transaction.

Public corporate records identify the Polish company as:

| Field | Data |

|---|---|

| Entity | Passpoint Sp. z o.o. |

| KRS | 0001139121 |

| NIP | 8762513363 |

| REGON | 540221384 |

| Registration Date | November 2024 |

Registry records also connect the company to:

- Kelechi Chidiebube Uchegbulem

- Adejuwon Samuel Oyebanjo

- Chinedu Bendeict Ojiteli

Passpoint’s public communications place strong emphasis on governance and compliance. In a May 2026 TechCabal interview, CEO Kelechi Uchegbulem stated that the real challenge in payment infrastructure is not simply moving money, but “governing it,” including routing logic, compliance obligations, FX exposure, and settlement predictability.

Key Findings

Passpoint Was the Visible Payee in Betify’s Deposit Rail

The May 2026 Betify investigation showed Passpoint Sp. z o.o. acting as the named payee within the open-banking deposit process. This indicates an active operational role rather than passive infrastructure exposure.

The Rail Connected Betify to Regulated Banking Infrastructure

The payment chain involved:

- InstantBankPayment

- Yapily Connect UAB

- Revolut

- Wise

- Passpoint Sp. z o.o.

This demonstrates that the casino funding flow touched regulated open-banking and banking infrastructure before reaching the final payee.

Payee Status Implies Operational Responsibility

If Passpoint acted as the payee, several compliance questions arise:

- Who onboarded the gambling merchant?

- Who controls settlement after receipt of funds?

- What contractual relationship exists between Passpoint and the underlying operator?

- Why was Passpoint displayed instead of the gambling merchant itself?

No Evidence of EU Payment Institution Authorization

Publicly available records identify Passpoint Sp. z o.o. as a Polish limited liability company with financial-services-related activity classifications and minimal share capital.

However, no publicly available evidence was identified showing authorization as:

- An EU payment institution

- An electronic money institution

- A licensed acquiring entity

- An authorized payment agent

This distinction is critical in high-risk sectors such as offshore gambling.

Registry Data Links the Entity to Passpoint Executives

Public company records associate the Polish entity with:

- Kelechi Uchegbulem

- Adejuwon Oyebanjo

- Chinedu Ojiteli

Registry documentation reportedly identifies Oyebanjo and Uchegbulem as shareholders, while Uchegbulem and Ojiteli appear as representatives.

Passpoint’s Compliance Narrative Raises Expectations

Passpoint markets itself as a compliance-oriented orchestration platform that combines:

- Payments

- Settlement

- Liquidity

- FX management

- Governance

- Compliance infrastructure

Because of that positioning, the company faces heightened scrutiny when appearing directly in high-risk gambling payment flows.

Standard Disclaimers Do Not Remove AML Obligations

Passpoint’s terms reportedly state that the company does not assume liability for the legality or quality of goods or services purchased through its infrastructure.

However, such disclaimers do not override obligations related to:

- AML monitoring

- Merchant due diligence

- Sanctions screening

- Licensing checks

- High-risk merchant onboarding

This becomes especially important in offshore gambling transactions.

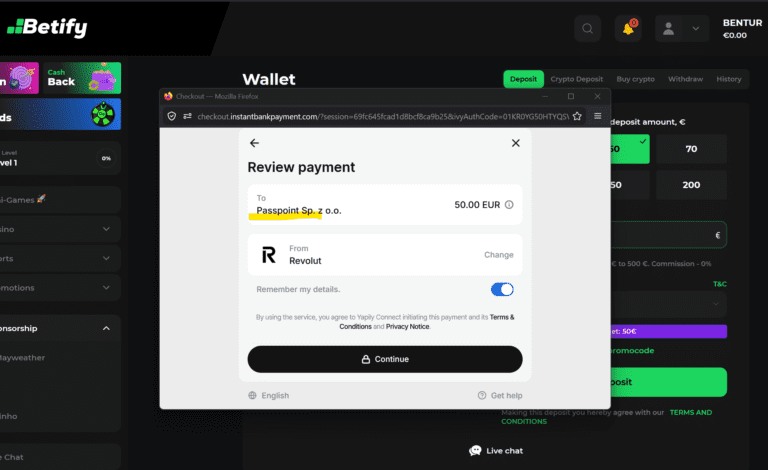

Betify Flow Shows Possible Merchant Masking

The customer intended to fund a Betify casino account, yet the visible payee shown in the transaction flow was Passpoint Sp. z o.o.

This discrepancy represents a classic payment-rail red flag because it may obscure the true merchant identity from:

- Banks

- Open-banking providers

- Monitoring systems

- Payment institutions

Overall Compliance Exposure Appears Significant

Unless Passpoint can provide evidence of:

- Proper licensing arrangements

- A lawful merchant-of-record structure

- Transparent settlement routing

- Compliant gambling merchant onboarding

the structure may raise concerns involving:

- Unlicensed payment intermediation

- Merchant masking

- Transaction laundering

Key Data Table: Passpoint

| Field | Information |

|---|---|

| Brand | Passpoint (LinkedIn page) |

| Main Domain | mypasspoint.com |

| Public Positioning | Financial orchestration platform for Africa, Europe, and G20 markets |

| Contracting Entity Mentioned | Passpoint Technologies Inc. |

| Claimed Services | Unified API for pay-ins, payouts, FX, liquidity, compliance, and settlement |

| U.S. Entity | Passpoint Technologies Inc. (Delaware, United States) |

| Polish Entity | Passpoint Sp. z o.o. |

| KRS / NIP / REGON | 0001139121 / 8762513363 / 540221384 |

| Linked Individuals | Adejuwon Oyebanjo (LinkedIn), Kelechi Uchegbulem (LinkedIn), Chinedu Ojiteli |

| Observed Payment Flow | Betify → InstantBankPayment → Yapily Connect UAB → Revolut / Wise → Passpoint Sp. z o.o. |

| Observed Role | Named Payee |

| Regulatory Concern | No publicly identified authorization as EU payment institution or payment agent |

Compliance Analysis

1. Payee Status Indicates an Active Transaction Role

The central issue is straightforward: Passpoint Sp. z o.o. appeared as the payee.

In open-banking systems, the payee is not an invisible backend vendor. The payee is the entity presented to the customer and banking infrastructure as the recipient of the funds.

That creates a critical question:

Why was Passpoint Sp. z o.o. displayed as the payee for a Betify casino deposit?

Its role strongly suggests involvement as:

- A payment-facing entity

- A settlement intermediary

- A merchant-of-record proxy

- A payment agent layer

2. Licensing Questions Are Fundamental

Passpoint Sp. z o.o. is registered as a Polish limited liability company. Public records do not demonstrate authorization as:

- A payment institution

- An EMI

- A licensed acquirer

- An authorized payment agent

If the entity collects or routes funds for third-party merchants — especially offshore casinos — it would generally require a valid regulatory basis.

In the gambling sector, the issue becomes even more sensitive. Payment providers cannot simply insert intermediary corporate payees into casino funding flows while claiming to be neutral API layers.

3. Merchant Masking and Transaction-Laundering Concerns

The economic purpose of the transaction was clear: funding a casino account at Betify.

However, the visible payee shown in the transaction chain was:

Passpoint Sp. z o.o.

not:

- Betify

- Fortuna Games N.V.

- Deltaprime Limited

This mismatch may obscure the actual gambling merchant from banks, payment providers, and monitoring systems.

In practical terms:

The customer funds Betify, but the banking system sees Passpoint.

This structure is commonly associated with merchant masking concerns and transaction-laundering risk analysis.

4. Passpoint’s Own Positioning Increases Compliance Expectations

Passpoint publicly promotes itself as a sophisticated financial orchestration platform covering:

- Compliance

- Cross-border settlement

- Payment governance

- Routing infrastructure

- Liquidity management

Its public messaging emphasizes control and oversight of payment flows.

Because of that positioning, the Betify findings raise more serious questions rather than reducing concern. A company claiming governance over payment flows must be able to explain:

- Merchant onboarding

- Risk categorization

- Settlement routing

- Compliance assessments

- Underlying payment purpose

5. Contractual Disclaimers Do Not Eliminate Regulatory Duties

Passpoint’s published disclaimers may attempt to distance the company from the underlying goods or services purchased through its infrastructure.

However, payment facilitators cannot contract away obligations tied to:

- AML compliance

- Merchant due diligence

- Sanctions controls

- Gambling-risk monitoring

- Licensing obligations

For gambling-related payments, processors are expected to know whether they are servicing:

- Authorized operators

- Offshore casinos

- Intermediary entities masking merchant identity

Why the Betify Rail Matters

The reviewed payment route was:

Betify → InstantBankPayment → Yapily Connect UAB → Revolut / Wise → Passpoint Sp. z o.o.

This structure immediately raises several important compliance questions:

- Who onboarded the underlying gambling merchant?

- Why was Passpoint selected as the visible payee?

- What legal basis supports this payment-facing role?

- Where are the funds ultimately settled?

- Were all payment providers aware the transfers funded offshore gambling activity?

Until these issues are clarified, the payment structure presents elevated regulatory and compliance risk indicators.

Conclusion

Passpoint’s appearance within the Betify payment chain cannot be dismissed as a harmless infrastructure artifact.

If Passpoint Sp. z o.o. appeared as the named payee, then the company acted as the visible recipient in a casino deposit transaction. That creates an immediate obligation to explain:

- The legal basis for the arrangement

- Licensing status

- Merchant onboarding procedures

- Settlement routing

- Risk and compliance controls

The issue is no longer whether Passpoint is an African fintech group with a Delaware parent and a Polish subsidiary. The key question is whether the Polish entity was used to collect or route EU player funds for an offshore casino without transparent merchant disclosure or appropriate payment authorization.

Until Passpoint provides a detailed explanation, Scam-Or Project classifies the company as a Very High Risk Rail Atlas Watchlist entity.

Scam-Or Project Whistleblower Request

Scam-Or Project invites players, PSP employees, bank insiders, compliance professionals, former Passpoint staff, open-banking specialists, and casino-payment insiders to share information regarding:

- Passpoint Technologies Inc.

- Passpoint Sp. z o.o.

- Kelechi Uchegbulem

- Adejuwon Oyebanjo

- Chinedu Bendeict Ojiteli

- Betify

- Fortuna Games N.V.

- Deltaprime Limited

- InstantBankPayment

- Yapily Connect UAB

- Revolut

- Wise

as well as related:

- Merchant agreements

- Settlement accounts

- Wallet infrastructure

- Onboarding files

- Banking relationships

Information may be submitted confidentially through the Scam-Or Project Complaints.