Revolut Rail Atlas: 1Go Casino Deposit Chain Routes Through BillBlend, SegoPay, Yapily, and CAPITOLIO

Offshore Casino Deposits Routed Into Open Banking Infrastructure

The latest Scam-Or Project Rail Atlas investigation into 1Go Casino demonstrates how offshore gambling platforms can move player deposits through several payment intermediaries before the transaction reaches a regulated open-banking environment.

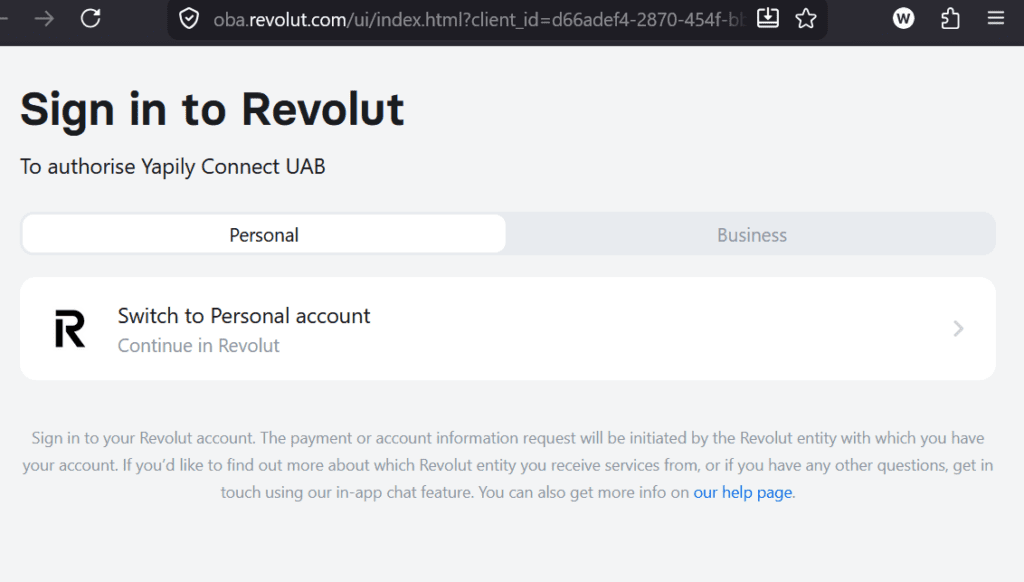

During the tested Revolut deposit flow, the payment sequence moved from the 1Go Casino cashier through BillBlend, SegoPay, Tryzto, InstantBankPayment, Yapily Connect UAB, and eventually to the Revolut Open Banking Authorization interface at oba.revolut.com.

At the final authorization stage, users were instructed to approve a payment initiated by Yapily Connect UAB. However, the visible beneficiary displayed on the payment review screen was neither 1Go Casino nor Galaktika N.V. Instead, the payee shown was CAPITOLIO INC.

Additional payment rails connected to the same casino environment displayed different beneficiaries, including Domus Payment Solutions and Galaktika N.V.

The investigation highlights a recurring structural weakness documented by the Scam-Or Project Rail Atlas initiative: casino deposits can be transformed into layered open-banking transactions where the regulated provider only becomes visible at the final authorization stage.

Key Findings

Dedicated Revolut Deposit Rail

1Go Casino provided a dedicated Revolut payment option. The tested route ultimately redirected users to oba.revolut.com, where authorization for Yapily Connect UAB was requested.

CAPITOLIO INC. Displayed as Beneficiary

The Revolut payment-review interface showed CAPITOLIO INC. as the recipient of a €25 payment. Neither 1Go Casino nor Galaktika N.V. appeared as the visible payee.

Multi-Layered Routing Structure

The observed transaction chain included multiple intermediary layers:

- pay.billblend.com/checkout

- tx.segopay.com/payment

- tryzto.com/ct/check

- checkout.instantbankpayment.com

- oba.revolut.com

Yapily Connect UAB at the Regulated Layer

At the final stage, Revolut displayed the message:

“Sign in to Revolut — To authorise Yapily Connect UAB.”

This confirms that the final payment-initiation layer relied on regulated open-banking infrastructure.

BillBlend and SegoPay as Upstream Processors

BillBlend appeared as the initial visible gateway, followed by SegoPay and additional routing layers before the payment reached the regulated banking interface.

InstantBankPayment Used Across Multiple Rails

The checkout.instantbankpayment.com infrastructure appeared in both the Revolut flow and separate Pay by Bank routes.

Different Rails, Different Beneficiaries

The reviewed payment flows displayed several different beneficiaries:

| Payment Rail | Visible Beneficiary |

|---|---|

| Revolut / Yapily | CAPITOLIO INC. |

| Pay by Bank / Wise | Domus Payment Solutions |

| MiFinity | Galaktika N.V. |

Multi-Rail Cashier Architecture

The cashier offered:

- Revolut

- MiFinity

- ByBit

- Crypto deposits

- Multiple Pay by Bank routes

This indicates a resilient offshore payment architecture with multiple fallback mechanisms.

Evidence Reviewed

The Scam-Or Project investigation reviewed payment-flow evidence collected during testing on May 5, 2026.

Reviewed Screenshots Included

- 1Go Casino cashier with deposit methods including Revolut, MiFinity, ByBit, Crypto Currency, and Pay by Bank.

- ByBit payment gateway page hosted under nczds3g4.fxcamyjxts.com/132882/.

- InstantBankPayment/Wise review screen showing a €25 payment to Domus Payment Solutions.

- MiFinity payment screen displaying Galaktika N.V. as beneficiary.

- Direct IBAN Pay by Bank screen requiring account-number input.

- InstantBankPayment bank-selection interface listing banks including Wise, Revolut, N26, ING, UniCredit, PostePay, and Intesa Sanpaolo.

- Revolut transition screen instructing users to continue payment via Revolut.

- Revolut/Yapily payment-review screen displaying CAPITOLIO INC.

- Revolut authorization page requesting approval for Yapily Connect UAB.

1Go Casino Cashier: Multi-Rail Deposit Infrastructure

At first glance, the 1Go Casino cashier resembles a typical offshore gambling payment interface with EUR-denominated balances, deposit limits, and bonus-code functionality.

However, the reviewed screenshots reveal a far more sophisticated payment-routing architecture.

Each payment option directs the user into a different operational flow involving distinct payment processors, beneficiaries, and infrastructure providers. This design is common among high-risk offshore gambling environments because it enables operators to maintain redundancy if one payment rail becomes unavailable.

The compliance concern is not merely the existence of multiple payment methods. The key issue is that the same casino deposit may ultimately be processed by entirely different entities depending on the selected rail.

Condensed Rail Overview

| Rail | Observed Path | Visible Beneficiary | Main Compliance Concern |

|---|---|---|---|

| Revolut / Yapily | 1Go → BillBlend → SegoPay → Tryzto → InstantBankPayment → Yapily Connect UAB → Revolut OBA | CAPITOLIO INC. | Casino deposit transformed into open-banking transaction with non-casino payee |

| Pay by Bank / Wise | 1Go → InstantBankPayment → Wise | Domus Payment Solutions | Corporate payee disconnected from casino branding |

| MiFinity | 1Go → MiFinity | Galaktika N.V. | Direct operator-linked beneficiary |

| ByBit / Crypto | 1Go → ByBit QR/app flow | Not confirmed | Potential movement outside traditional banking oversight |

| Direct IBAN Route | 1Go → IBAN/account form | Not confirmed | Additional fallback infrastructure |

Revolut Flow: Casino Deposit Becomes Open-Banking Authorization

The Revolut route remains the most significant finding in this Rail Atlas review.

The tested flow proceeded as follows:

1Go Casino

→ BillBlend

→ SegoPay

→ Tryzto

→ InstantBankPayment

→ Revolut OBA

→ Yapily Connect UAB authorization

At the final stage, the user no longer encountered a visible casino payment interface. Instead, the process appeared as an open-banking authorization request involving Yapily Connect UAB.

This demonstrates how offshore gambling transactions can be transformed into regulated payment-initiation flows only visible at the final stage of the customer journey.

The concern is not simply the presence of Revolut as a payment method. The central issue is the layered routing structure that separates the original gambling context from the regulated banking authorization interface.

CAPITOLIO INC. Appears as Revolut Beneficiary

One of the most important observations was the appearance of CAPITOLIO INC. as the visible beneficiary during the Revolut/Yapily payment flow.

The payment-review screen did not display:

- 1Go Casino

- Galaktika N.V.

- BillBlend

- SegoPay

- InstantBankPayment

Instead, the €25 payment beneficiary was listed as CAPITOLIO INC.

Publicly available information indicates that CAPITOLIO presents itself as a Canadian payment and digital-asset infrastructure provider registered with FINTRAC as a Money Services Business under registration number M24928320.

The company advertises services including:

- Open-banking payments

- Fiat-to-crypto infrastructure

- Account-to-account transfers

- Digital asset services

- Gaming-related payment support

Its role in the reviewed 1Go Casino flow therefore raises substantial compliance questions.

The central issue is straightforward:

Why did a player deposit initiated inside an offshore casino environment end up as an open-banking payment to CAPITOLIO INC. rather than directly to the casino operator?

BillBlend and SegoPay as Upstream Routing Layers

The first visible gateway in the tested flow was:

pay.billblend.com/checkout

BillBlend appears to operate as an upstream payment gateway for high-risk merchants, including gaming-related businesses.

The next routing stage was:

tx.segopay.com/payment

SegoPay has previously appeared in connection with high-risk gambling payment infrastructure and currently holds a “black” rating on RatEx42.

The compliance concern is not merely the involvement of these entities individually, but their collective role within the routing chain before the payment reaches regulated banking infrastructure.

This layered structure may reduce visibility into the original purpose of the transaction by the time the payment reaches the banking authorization stage.

Opaque Gateway Infrastructure and Domus Payment Solutions

After BillBlend and SegoPay, the tested flow passed through:

- tryzto.com/ct/check

- checkout.instantbankpayment.com

These layers appeared largely opaque from a consumer perspective. The reviewed interfaces did not clearly disclose the full merchant structure or explain the relationship between the casino, payment processors, and ultimate beneficiaries.

InstantBankPayment appeared across multiple rails.

In the Pay by Bank/Wise route, the beneficiary shown was Domus Payment Solutions.

Public records associate Domus Payment Solutions LTD (website) with Canadian wallet and payment infrastructure services involving:

- Currency exchange

- Wallet accounts

- Payment processing

- Crypto-related functionality

Public FINTRAC-related notices also indicate that Domus Payment Solutions Ltd.’s MSB registration was revoked during the 2022–2023 Q4 period.

Its appearance as a beneficiary within a casino payment flow raises additional questions regarding merchant onboarding, transaction monitoring, and gambling-payment classification.

MiFinity Rail Directly Displayed Galaktika N.V.

Unlike the other reviewed rails, the MiFinity payment route displayed Galaktika N.V. as beneficiary.

Public casino listings identify Galaktika N.V. as the apparent operator associated with 1Go Casino.

This creates a notable contrast:

| Rail | Beneficiary |

|---|---|

| MiFinity | Galaktika N.V. |

| Pay by Bank / Wise | Domus Payment Solutions |

| Revolut / Yapily | CAPITOLIO INC. |

The structure suggests a multi-beneficiary payment architecture where different entities may act as payees depending on the selected deposit rail.

Compliance Analysis

1. Merchant Opacity

The same casino cashier produced multiple different beneficiaries depending on the selected rail.

This makes it difficult for:

- players,

- banks,

- regulators,

- payment providers,

- compliance teams

to clearly identify who is actually receiving player funds.

2. Payment-Purpose Dilution

The original purpose of the transaction is evident: a player deposits funds into a gambling account.

However, by the time the payment reaches the banking layer, the visible payee may appear unrelated to gambling.

This creates a risk that the transaction is monitored as an ordinary corporate transfer instead of a gambling payment.

3. Open-Banking Misuse Risks

Open banking was designed for efficient account-to-account payments.

In high-risk environments, however, it may function as a chargeback-resistant gambling funding mechanism.

Unlike traditional card payments, open-banking transfers may provide consumers with fewer recovery mechanisms.

4. Regulated Chokepoints

The final stages of the reviewed flow involved regulated entities:

- Yapily Connect UAB

- Revolut OBA

This does not automatically imply wrongdoing by those providers.

However, it confirms that regulated infrastructure appeared at the end of a payment chain originating inside an offshore casino environment.

5. Resilient Multi-Rail Architecture

1Go Casino appears to operate a robust multi-rail payment system that includes:

- open banking,

- crypto,

- wallet services,

- app-based payment flows,

- IBAN transfers.

Such structures allow operators to reroute users between alternative payment channels if one becomes restricted or unavailable.

Conclusion

The reviewed 1Go Casino payment structure provides another detailed example of how offshore gambling operators can route player deposits through layered payment infrastructure before the transaction reaches regulated banking systems.

The issue is not simply that Revolut or open banking is offered as a deposit option.

The core issue is that a gambling deposit originating inside a casino cashier can pass through multiple routing layers — including BillBlend, SegoPay, Tryzto, InstantBankPayment, Yapily Connect UAB, and Revolut OBA — before the final beneficiary appears as a separate non-casino entity such as CAPITOLIO INC.

The same pattern appears in other rails involving Domus Payment Solutions.

This creates a structural compliance risk:

By the time the payment reaches the regulated banking layer, the original gambling context may no longer be visible.

For banks, regulators, payment institutions, and open-banking providers, the critical question is becoming increasingly clear:

Can existing monitoring systems reliably identify these transactions as gambling-related deposits once they have been routed through intermediary gateways and relabeled under alternative beneficiary names?

If not, open banking may increasingly function as a high-risk offshore casino funding mechanism rather than merely a payment innovation.

Scam-Or Project will continue mapping these payment rails and identifying the payment processors, gateway operators, beneficiaries, and regulated chokepoints involved in such transaction structures.

Whistleblower Call

Scam-Or Project invites:

- players,

- payment insiders,

- former employees,

- compliance officers,

- PSP staff,

- open-banking specialists

to provide additional information regarding:

- 1Go Casino

- Galaktika N.V.

- CAPITOLIO INC.

- Domus Payment Solutions

- BillBlend

- Fin&Pay Partners OÜ

- SegoPay

- Tryzto

- InstantBankPayment

- Yapily Connect UAB

- Revolut OBA

- MiFinity

- ByBit

- related casino payment flows

Relevant materials may include:

- screenshots,

- payment confirmations,

- URLs,

- gateway redirects,

- merchant descriptors,

- bank statements,

- GDPR responses,

- onboarding documentation,

- KYC records,

- internal compliance communications.

Information can be submitted confidentially through the Scam-Or Project Complaints.