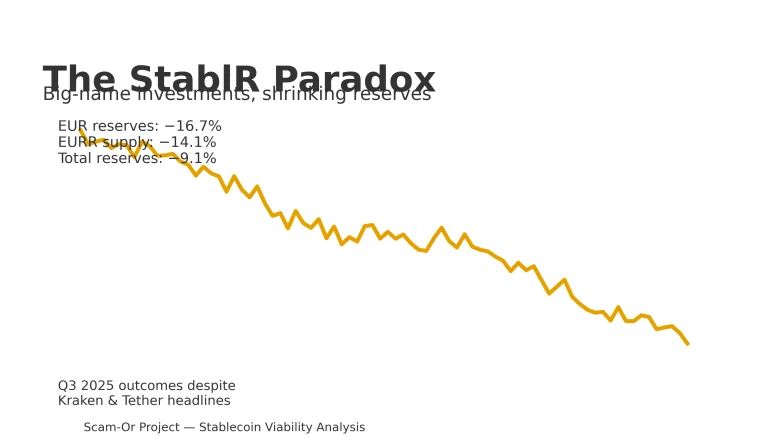

Strategy’s “BTC Yield” After the Latest 196-BTC Purchase: What the Per-Share Math Really Says

Snapshot

Strategy (formerly MicroStrategy) disclosed another incremental buy—196 BTC for roughly $22.1 million—cementing its reputation as the flagship corporate Bitcoin treasury. The headline is bullish, but the metric that truly governs long-run shareholder value—“BTC yield”—has been slowing, largely because capital raised has recently outpaced net coins deployed, with a portion of proceeds diverted to preferred-stock obligations. For investors, the key lens isn’t “how many coins,” but Bitcoin-per-share (BPS) accretion and its momentum over time. (Source: Coincentral)

Reframing “BTC Yield”

Working definition. BTC yield is the percentage change in BPS over a chosen interval.

-

BPS (Bitcoin per share) = total BTC on the balance sheet ÷ diluted shares outstanding.

-

When BPS increases, each common share is backed by more BTC.

-

When new issuance (equity/convertibles/preferreds) grows faster than BTC acquired, BPS rises more slowly—or stalls.

Why this governs value. Strategy’s financing engine (ATMs, converts, preferreds) can expand BTC exposure, but dilution can offset the stacking. Only net coins added per share compound value for common stockholders. Management has highlighted “BTC yield” snapshots YTD to draw attention to this per-share lens. (Sources: Investopedia, X)

How Strategy Runs Its Treasury (as tracked by Scam-Or Project)

Core mandate. Operate as a Bitcoin Treasury Company: raise capital opportunistically, buy weakness, and hold. The rebrand from MicroStrategy to Strategy Inc. formalized the mission.

Purchase rhythm. The firm has favored smaller, frequent tickets—most recently 196 BTC at about $113k/BTC—which keeps the stacking narrative alive. However, relative to recent fundraising scale, these adds are modest, putting downward pressure on BTC yield when proceeds are not predominantly converted into BTC. (Source: Strategy)

The Four Numbers That Matter

| KPI | What It Captures | Practical Implication |

|---|---|---|

|

Total BTC |

Aggregate coins on the balance sheet |

Good headline, but ignores share growth |

|

Diluted Shares |

Common + in-the-money converts/options |

Rising denominator can mute BPS |

|

BPS (BTC/share) |

Total BTC ÷ diluted shares |

True per-share exposure to BTC |

|

BTC Yield (ΔBPS%) |

% change in BPS over time |

Clean gauge of shareholder-level stacking |

Funding mix check. When a slice of capital must service preferred dividends or operating needs, less cash reaches BTC, slowing ΔBPS even if total coins rise.

Tailwinds vs. Headwinds

Where the Wind Helps

-

Levered BTC beta. Historically, Strategy’s equity can outperform spot BTC in bull phases due to balance-sheet gearing and narrative premium.

-

Accounting clarity (2025). Adoption of fair-value accounting should reduce impairment noise and surface mark-to-market BTC impacts more cleanly in GAAP reporting.

Where the Wind Fights Back

-

Decelerating BTC yield. If issuance > BTC deployment, BPS growth cools, softening the core per-share thesis for common holders.

-

NAV-premium sensitivity. A narrowing premium (price vs. look-through BTC value) raises the cost of equity funding, potentially slowing future accumulation and ΔBPS.

Source: ft.com

Interpreting the Latest 196-BTC Add

Another buy reinforces the “corporate BTC treasury” narrative, but sophisticated analysis should weight per-share math over aggregate coins. The direction and pace of BPS and BTC yield—plus financing mix and any premium/discount to NAV—are the decision drivers for equity holders. (Source: Bitcoin Treasuries)

Investor To-Dos

-

Track BPS and ΔBPS (BTC yield) each quarter; treat “BTC purchased” as context, not the core.

-

Inspect proceeds flow. If preferred dividends or opex absorb more cash than expected, anticipate a slower BTC yield print.

-

Portfolio construction. Strategy remains the marquee BTC-treasurer:

-

Want pure BTC? Hold BTC.

-

Want levered BTC with equity optionality? Consider MSTR, but size positions for volatility in BTC yield and NAV-premium swings.