The Banking Paradox: How Tier-1 European Banks May Be Helping Illegal Offshore Casinos Survive Through Transaction Laundering Blind Spots

Overview

As European gambling regulators escalate enforcement against illegal offshore casino operators, a more difficult question is surfacing for the banking sector: are major retail banks, through rigid dispute practices and limited scrutiny of miscoded card payments, indirectly allowing these gambling networks to keep functioning?

Complaints involving shell merchants, misleading Merchant Category Codes (MCC), and rejected chargebacks point to a broader compliance gap that may warrant closer attention from financial regulators.

Key Findings

- Major retail banks may be processing card transactions connected to illegal offshore casinos through shell merchants using allegedly misleading MCC classifications.

- Payments that should trigger immediate AML and card-scheme concerns can appear on statements as purchases of digital goods or standard retail transactions rather than gambling activity.

- Consumers who disclose the true gambling background of a transaction reportedly face a higher risk of dispute rejection, even where there are indications of miscoding or transaction laundering.

- This creates a distorted incentive structure in which honest reporting may reduce the likelihood of recovery, while vague commercial complaints such as “goods not delivered” may be treated more favorably.

- The apparent disconnect between internal bank dispute handling, card-scheme obligations, and AML expectations deserves attention from financial supervisors, not only gambling authorities.

A Question Regulators Still Need to Address

Across Europe, regulators are intensifying action against illegal offshore gambling platforms. National authorities are issuing public warnings, imposing fines, and ordering access restrictions against unlicensed casino sites aimed at local users. However, one major issue remains insufficiently explored: how are deposits to these operators still moving so smoothly through mainstream banking channels?

According to information shared with Scam-Or Project, part of the answer may lie in the overlap between card acquiring, dispute procedures, and compliance weaknesses at major European retail banks.

The core allegation is not that banks openly support illegal gambling. The more serious concern is that some institutions, including Revolut, may be structurally overlooking obvious signs of transaction laundering and merchant misrepresentation, thereby allowing illegal offshore casino ecosystems to operate in plain sight.

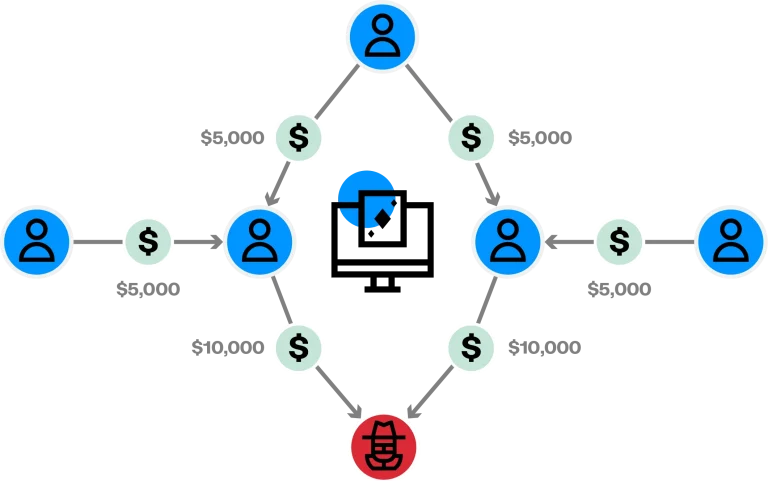

The Hidden Payments Infrastructure Behind Offshore Gambling

When a consumer deposits money with an offshore casino, the payment does not always appear as gambling-related. Instead, the charge may be routed through an intermediary merchant or shell company presenting itself as a software vendor, digital goods seller, e-commerce merchant, or another seemingly harmless commercial business.

In these situations, the payment may be processed under an MCC other than the gambling code 7995. Market participants and affected consumers have repeatedly pointed to MCC 5816 and similar retail-style classifications as examples of how gambling-related transactions may be disguised.

Regulators and supervisors have already warned about illegal gambling payment exposure, shell or sub-merchant opacity, and transaction laundering. Yet the role of misleading or false MCC allocation in helping such flows bypass bank controls has received far too little attention. This issue has also been touched on in the Dutch DNB publication Gambling and Gaming Good Practices for Payment Institutions and Good Practices Sub-Merchants.

From a compliance standpoint, this is not a marginal technical irregularity. Where a gambling payment is disguised through a false merchant identity and misleading MCC coding, the conduct may amount to transaction laundering. It is also a serious indicator of AML, KYC, and card-scheme risk.

Why the Chargeback Stage Is So Important

The issue becomes especially visible when the customer later attempts to dispute the transaction.

A recurring scenario described to Scam-Or Project is the following: a consumer deposits funds with an offshore casino, then loses access to the account, encounters withheld winnings, or discovers that the merchant descriptor on the card statement does not match the actual service used. The customer then contacts the issuing bank to request a chargeback.

At that point, the dispute may allegedly be reviewed not through the lens of merchant misrepresentation, transaction laundering, or card-scheme compliance, but through a simplified internal logic: the customer intended to gamble, the funds reached the casino environment, therefore the service was delivered and the dispute must be rejected.

That is more than a customer-service failure. It may reflect a deeper structural problem: the bank may be declining to assess whether the merchant identity was false, whether the MCC was manipulated, whether the acquirer onboarded the merchant correctly, and whether the overall payment chain was deliberately designed to evade gambling controls.

Compliance Red Flags Banks Should Be Examining

From an AML and card-compliance perspective, several warning signs should trigger enhanced review:

1. Merchant Description Mismatch

The merchant shown on the customer’s statement reportedly does not match the casino brand the consumer actually used.

2. Suspicious MCC Allocation

The payment may be coded as digital goods, software, or standard retail rather than gambling, even though the underlying transaction relates to casino activity.

3. Use of Shell Companies

The named merchant is often a little-known corporate entity with no genuine public-facing business activity consistent with the transaction description.

4. Dispute Logic Detached From Merchant Reality

Rather than examining whether the transaction was truthfully represented, banks may focus only on the customer’s intention to gamble.

5. Possible Card-Scheme Rule Evasion

Where the acquiring documentation, merchant identity, and represented service do not align, the case may involve card-scheme compliance issues, not merely customer dissatisfaction.

These are not fringe concerns. They sit at the center of AML controls, merchant due diligence, and the integrity of the card-payment system.

The Perverse Incentive: Honest Consumers May Be Penalized

Perhaps the most troubling aspect of these allegations is the incentive structure they appear to produce.

Consumers report that when they fully disclose the offshore casino context in an effort to expose merchant deception, banks may reject the dispute on policy or moralistic grounds connected to gambling. Yet when the same transaction is framed in generic commercial language — for example, as software or digital goods not delivered — the dispute may stand a better chance of succeeding, simply because the shell merchant cannot prove delivery of the claimed product.

That creates a deeply problematic result: banks may be discouraging honest reporting while unintentionally rewarding concealment.

In other words, the current system may be better equipped to process simplified complaint scripts than to confront potential transaction laundering.

For related payment-risk concerns, read our report on Revolut here.

A Regulatory Blind Spot That Goes Beyond Gambling

This is precisely why the issue should not remain limited to gambling regulators.

Authorities such as the Dutch KSA, the UK Gambling Commission, and other national gambling watchdogs can act against unlicensed casino operators. But they do not oversee the internal dispute-handling logic of major retail banks. That is where financial regulators and AML supervisors come into play.

The real question is whether retail banks and their card-dispute teams are adequately trained, required, and incentivized to identify transaction laundering indicators when consumers provide evidence of merchant mismatch, misleading MCC coding, and shell-company routing.

If the answer is no, banks risk becoming passive infrastructure providers for illegal gambling networks while publicly maintaining a zero-tolerance posture.

Why ING, Rabobank, and Other Banks Merit Closer Review

The institutions identified by the source, including ING and Rabobank, are not presented here as proven wrongdoers. However, they are cited as examples of major banks whose internal handling of these complaints may deserve closer examination.

For Scam-Or Project, the central issue is whether the alleged shortcomings are isolated case-management failures or signs of a broader structural pattern across European retail banking.

If dispute teams are systematically ignoring transaction laundering indicators simply because the consumer was involved in gambling, that would amount to a serious governance problem. It would also raise difficult questions about how banks interpret their obligations under AML frameworks, card-scheme rules, and consumer-protection standards.

Preliminary Assessment

The information reviewed by Scam-Or Project suggests a potentially significant enforcement gap at the intersection of illegal gambling, acquiring, retail banking, and card-dispute operations.

Even where a consumer knowingly interacted with a gambling website, that does not remove the need to examine whether the transaction was deceptively presented, processed through a false merchant, or intentionally miscoded to avoid controls. A bank that refuses to assess those elements may be overlooking exactly the type of conduct that AML and card-compliance frameworks are supposed to detect.

This is not just a consumer-rights matter. It may also be a payment-integrity problem.

Risk Indicators at a Glance

| Risk Area | Description | Why It Matters |

|---|---|---|

| Merchant mismatch | Statement descriptor differs from actual casino brand | May indicate merchant misrepresentation |

| False MCC coding | Gambling-related payment coded as retail or digital goods | Can help transactions evade controls |

| Shell merchant use | Payment routed through opaque corporate entity | Raises AML and KYC concerns |

| Narrow dispute logic | Bank focuses only on gambling intent | May ignore transaction laundering indicators |

| Scheme-rule inconsistency | Merchant identity, service, and acquiring data do not match | Suggests broader compliance failure |

Call for Whistleblowers and Insiders

Scam-Or Project is investigating how banks, acquirers, PSPs, and card-dispute teams handle suspicious card transactions linked to illegal offshore casinos, shell merchants, and false MCC coding.

Insiders, compliance officers, former dispute-team staff, acquirer employees, payment specialists, and affected consumers are invited to share information, documents, merchant descriptors, chargeback correspondence, or internal guidance through the Scam-Or Project website.

If you have evidence of transaction laundering, miscoded gambling transactions, shell merchants, or internal bank policies that systematically ignore these warning signs, your information may help clarify a significant blind spot in Europe’s financial compliance system.