Dutch Player Reveals Paysolo, Pellopay, Impaya and a Revolut Open-Banking Casino Corridor

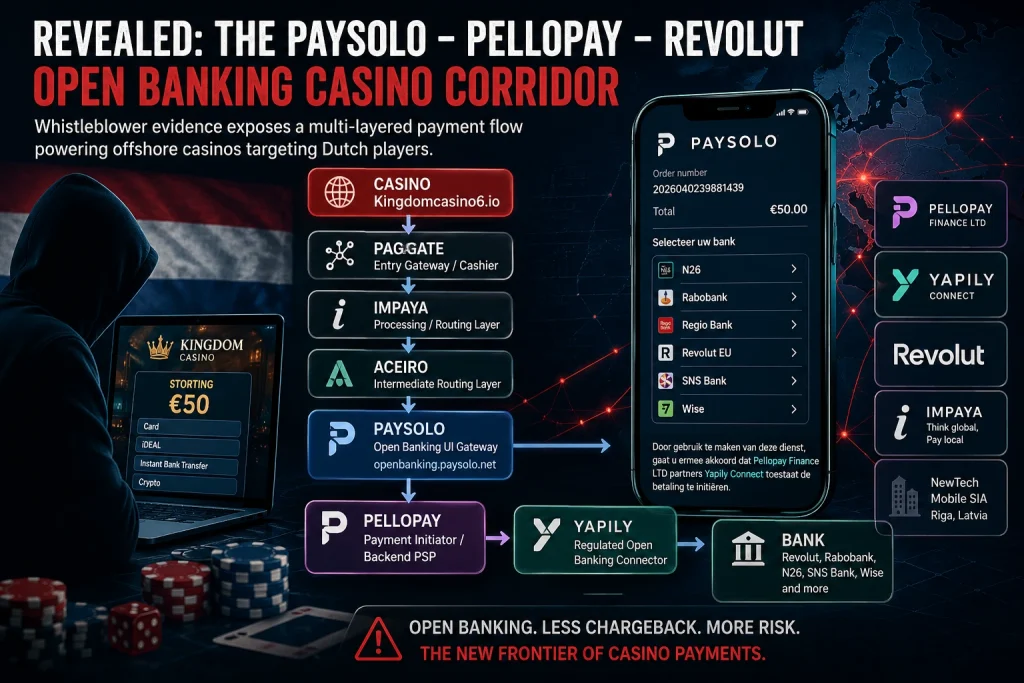

Fresh whistleblower material reviewed by Scam-Or Project points to a Dutch-targeted casino deposit route that begins at Kingdomcasino and ultimately reaches an open-banking interface hosted on openbanking.paysolo.net. At this stage, users are presented with banking options including Revolut, Rabobank, N26, SNS Bank, and Wise.

The payment page itself includes a consent notice stating that users authorize “Pellopay Finance LTD partners Yapily Connect” to initiate the transaction. This evidence further supports Scam-Or Project’s working theory that layered infrastructures—anonymous gateways, open-banking providers, fiat-to-crypto bridges, and APIs like Revolut’s—can form complex casino payment corridors.

Key Findings

-

Video evidence captures a real deposit flow

The journey starts on kingdomcasino6.io, displaying a €50 deposit page in Dutch with options such as card, iDEAL, instant bank transfer, and crypto. -

Redirection to Paysolo interface

The process continues to openbanking.paysolo.net, where the Paysolo logo, order ID (2026040239881439), and €50 total are shown, along with a Dutch-language bank selection interface. -

Revolut EU listed among bank options

Available banks include N26, Rabobank, Regio Bank, Revolut EU, SNS Bank, and Wise. -

Pellopay and Yapily referenced in consent layer

The footer confirms that users agree to allow Pellopay Finance LTD, in cooperation with Yapily Connect, to initiate payments. -

Yapily’s positioning in iGaming

Yapily promotes open-banking solutions tailored for iGaming, supporting both consumer and business transactions. -

Regulatory footprint of Yapily Connect

Public data shows Yapily Connect Ltd operates as a regulated open-banking provider across 19 countries. -

Impaya and NewTech Mobile SIA linkage

Latvian corporate records identify NewTech Mobile SIA (registration no. 40103709254, Riga) as potentially connected to Impaya. -

Impaya’s positioning

The company markets itself as a full-service e-commerce payment solution provider.

Observed Payment Flow

Based on the video and screenshots, the transaction path appears to follow this structure:

Kingdomcasino6.io → payment interface / possible Impaya-linked layer → openbanking.paysolo.net → Pellopay / Yapily Connect consent layer → bank selection → Revolut EU and other banks

While this does not establish contractual liability for each participant, it clearly demonstrates a functioning deposit journey that passes through Paysolo’s open-banking gateway and references Pellopay, Yapily Connect, and Revolut EU.

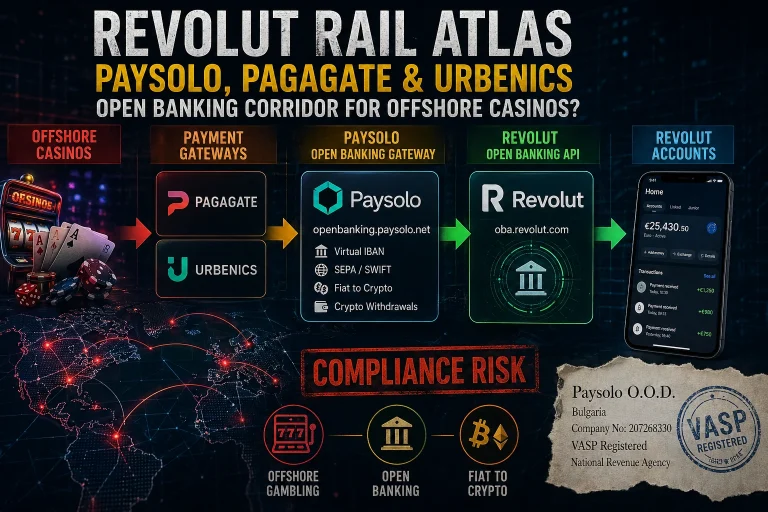

From Casino to Bank: A Multi-Layered Payment Chain

The evidence suggests that openbanking.paysolo.net acts as the user-facing interface, while Pellopay Finance LTD operates at the consent and initiation layer.

Payment Chain Overview

- Casino

- Pagagate (entry gateway / cashier)

- Impaya (processing / routing layer)

- Aceiro (intermediate routing layer)

- Paysolo (open banking interface)

- Pellopay (payment initiator / backend PSP)

- Yapily (regulated open-banking connector)

- Bank (Revolut, Rabobank, etc.)

This layered architecture indicates a fragmented orchestration model, where separate entities manage access, routing, and execution. Such fragmentation can obscure the merchant’s identity before funds reach regulated banking systems.

Public information suggests Pellopay Finance Ltd, a Canada-registered processor, provides API-driven payment solutions, including bank transfers, wallets, and Revolut integration. This aligns with its apparent backend role, while Yapily provides regulated connectivity.

Evidence & Confidence Table

| Entity / Rail Element | Observed Role | Evidence Type | Confidence |

|---|---|---|---|

| Kingdomcasino | Casino deposit origin | Uploaded video | Corroborated |

| Paysolo / openbanking.paysolo.net | Bank selection interface | Video + screenshot | Confirmed |

| Revolut | Listed bank option | Video + screenshot | Confirmed |

| Pellopay Finance LTD | Consent layer payment initiator | Video + screenshot | Confirmed |

| Yapily Connect | Open-banking partner | Video + public records | Corroborated |

| Impaya | Payment routing layer | Whistleblower statement | Indicated |

| NewTech Mobile SIA | Possible EU representative | Statement + registry data | Indicated |

| Aceiro | Referenced routing alias | Whistleblower statement | Indicated |

Compliance Analysis

1. Open Banking vs Chargeback Protection

Payments via open banking may bypass traditional card chargeback mechanisms. In gambling scenarios—where disputes and blocked withdrawals are common—this significantly reduces consumer protection.

2. Yapily and iGaming Exposure

Yapily openly supports iGaming payments. While legal in regulated markets, the presence of its infrastructure in offshore casino flows targeting Dutch users raises compliance concerns.

3. Revolut as Downstream Endpoint

Revolut appears as a selectable bank within the Paysolo interface. This does not confirm a direct relationship with the casino but demonstrates that payment routing can end within Revolut’s ecosystem.

4. Paysolo as Conversion Layer

Paysolo plays a key role at the moment of transaction confirmation. Previous Rail Atlas findings already linked it to flows involving Pagagate, Urbenics, and oba.revolut.com. This case adds concrete transaction-level evidence.

Key Questions for Involved Parties

Paysolo

- Is Paysolo the operator of openbanking.paysolo.net?

- Does it process payments for Kingdomcasino6.io, Luckzie.io, Jinxcasino.io, Pagagate, Urbenics, Impaya, Aceiro, or Pellopay?

- Are upstream merchants screened for gambling activity and licensing compliance?

Pellopay

- What exact role does Pellopay Finance LTD play in this flow?

- Is it acting as PSP, merchant, or technical provider?

- Does it onboard or monitor gambling-related clients?

Yapily

- Was Yapily Connect directly involved in the captured transaction?

- Does it permit usage in offshore casino environments targeting Dutch users?

- What merchant data is passed to banks like Revolut?

Revolut

- Can Revolut identify that these flows originate from casino deposits?

- Are entities such as Paysolo, Pellopay, Impaya, Pagagate, or Urbenics flagged as high-risk?

- Are payments to unlicensed operators blocked?

Impaya / NewTech Mobile / Aceiro

- What role do these entities play in routing or gateway services?

- Who is the merchant of record in the observed transaction?

Conclusion

The newly obtained evidence provides a clearer, transaction-level view of how a casino deposit flow can move through multiple intermediaries before reaching regulated banking infrastructure.

The flow demonstrates that Paysolo, Pellopay Finance LTD, Yapily Connect, and Revolut EU can all appear within a single payment journey. While this does not confirm deliberate involvement by any specific entity, it highlights how open-banking systems can be embedded into casino payment processes in ways that:

- obscure the underlying merchant

- limit chargeback protections

- shift financial risk into account-to-account payment rails

For regulators, the implication is straightforward: the critical control point for casino payments is no longer limited to card acquiring—it has shifted toward open-banking ecosystems.