Processor-as-Payee Casino Rails: How Open Banking Structures Can Obscure Gambling Deposits and Undermine Player Refund Rights

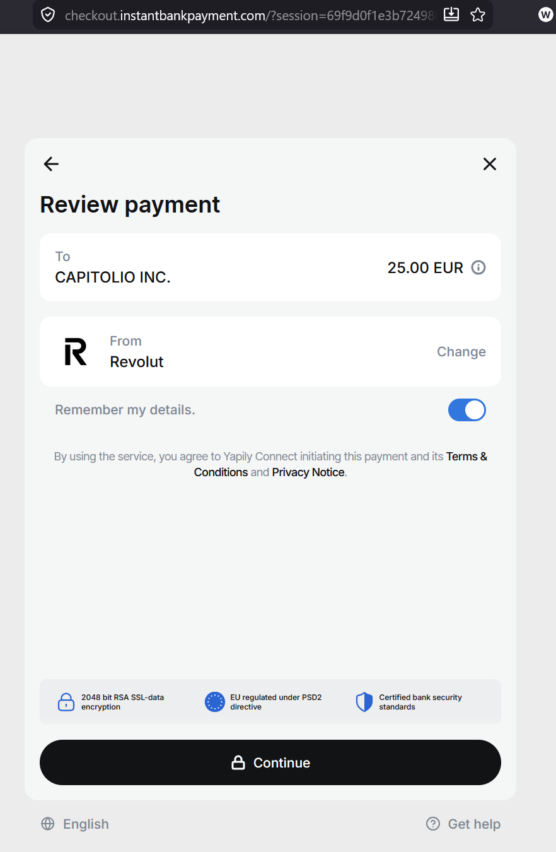

Recent Scam-Or Project Rail Atlas investigations into offshore casino payment flows reveal a recurring and highly controversial structure: a player initiates a casino deposit, but the bank-facing payment screen identifies a payment processor — such as CAPITOLIO INC. or Domus Payment Solutions — instead of the actual gambling operator.

While this may appear to be a technical implementation detail, the consequences are potentially significant. In traditional card payments, consumers may still benefit from chargeback procedures and dispute mechanisms. In contrast, Pay-by-Bank and open-banking account-to-account (A2A) transfers provide materially weaker recovery options. This creates a major consumer-protection issue: if the casino operator disappears behind intermediary payment entities, how can players realistically enforce refund or restitution claims against unauthorised gambling platforms?

Executive Summary

Scam-Or Project’s recent Rail Atlas reviews involving offshore casino cashiers — including 1Go Casino and Winnita — identified a repeating payment structure:

- the user initiates what is clearly a casino deposit;

- intermediary payment gateways and open-banking providers process the transaction;

- the final payee shown on the bank-facing screen is a processor or infrastructure company rather than the casino itself.

In the 1Go Casino payment review, CAPITOLIO INC. appeared as the payee within a Revolut/Yapily open-banking rail, while Domus Payment Solutions appeared in a separate Pay-by-Bank setup.

In the Winnita payment investigation, Scam-Or Project again identified Domus Payment Solutions as the visible payee in a flow involving InstantBankPayment, Token GmbH/Token.io, and Revolut.

This distinction matters because open-banking transfers operate differently from card-based transactions. They bypass traditional card-network infrastructure and therefore do not include standard chargeback protections. Industry documentation consistently describes refund and dispute resolution as dependent on merchant policies and the safeguards implemented by the payment-initiation provider.

Why Timing Matters: Recent CJEU Gambling Judgments

Recent judgments from the Court of Justice of the European Union (CJEU) have increased the importance of payment transparency in gambling disputes.

Case C-440/23

In Case C-440/23, involving European Lotto and Betting and Deutsche Lotto- und Sportwetten, the CJEU confirmed that EU law does not prevent Member States from enforcing national gambling restrictions, even when an operator holds a licence in another EU jurisdiction.

The proceedings specifically addressed:

- recovery of gambling losses,

- abuse-of-law arguments,

- online slot-machine operations,

- cross-border authorisation issues.

The judgment confirmed that Member States may attach civil-law consequences — including restitution claims — to gambling services offered without the required local authorisation.

Case C-77/24 Wunner

In Case C-77/24 Wunner, the Court examined cross-border liability claims related to unlicensed gambling operators and clarified the relevance of the player’s country of residence or participation when determining jurisdiction and applicable law.

Legal commentary surrounding the judgment indicates that players may often rely on the law of their habitual-residence Member State when pursuing claims against foreign gambling operators lacking proper local licensing.

Against this legal background, processor-as-payee payment structures become particularly problematic. If players cannot clearly identify the actual gambling operator or beneficiary within the payment flow, enforcing restitution rights may become practically difficult — even where national law formally allows recovery claims.

Key Findings

1. Processor-as-Payee Structures Are Repeatedly Appearing

Scam-Or Project identified processor-as-payee structures across multiple offshore casino payment flows:

| Casino | Observed Payee | Payment Flow |

|---|---|---|

| 1Go Casino | CAPITOLIO INC. | Revolut/Yapily open banking |

| 1Go Casino | Domus Payment Solutions | Pay-by-Bank rail |

| Winnita | Domus Payment Solutions | InstantBankPayment + Token.io + Revolut |

2. The Casino Operator Often Disappears From the Payment Screen

Although the player initially interacts with a casino-branded cashier page, the visible beneficiary shown during the banking authorisation stage may instead be:

- a payment processor;

- a wallet provider;

- a collection entity;

- an MSB;

- or another infrastructure intermediary.

3. The Structure Is Not Automatically Illegal

A processor can legally appear as:

- merchant of record;

- payment facilitator;

- collection agent;

- technical settlement provider.

However, in gambling-related payment flows, this model only remains defensible if:

- the true gambling merchant is transparently disclosed;

- the payment purpose remains identifiable;

- refund and complaint procedures are clear;

- licensing status is properly verified;

- transaction monitoring preserves gambling-related context.

4. Payment-Purpose Dilution Is the Core Risk

A major concern is what Scam-Or Project describes as “payment-purpose dilution.”

The transaction begins as a gambling deposit but may ultimately appear within banking systems as an ordinary transfer to a payment infrastructure company. This weakens visibility into the true economic purpose of the payment.

5. Open Banking Weakens Traditional Recovery Options

Unlike card-based systems, open-banking A2A payments do not rely on card-network infrastructure. As a result:

- no universal chargeback mechanism exists;

- disputes depend heavily on merchant cooperation;

- players may struggle to recover funds after disputes or casino shutdowns.

The Observed Payment Architecture

Typical Processor-as-Payee Casino Flow

| Layer | Player Sees | Observed Infrastructure | Compliance Concern |

|---|---|---|---|

| Casino Cashier | 1Go Casino / Winnita | Gambling purpose visible initially | Gambling context initially obvious |

| Gateway Layer | InstantBankPayment, BillBlend, SegoPay, Tryzto | Casino branding diluted | Intermediaries obscure merchant |

| Open-Banking Layer | Yapily, Token.io, Bridge/SaltEdge | PISP infrastructure | A2A payment initiation |

| Bank Authentication | Revolut, Wise, other banks | Customer authorises payment | Push-payment execution |

| Visible Payee | CAPITOLIO INC. / Domus Payment Solutions | Non-casino entity displayed | Merchant substitution risk |

| Final Destination | Casino balance credited | Ultimate beneficiary unclear | Transparency concerns |

The issue is not the existence of processors themselves. Payment processors are standard across digital commerce. The problem arises when the visible merchant changes between the casino interface and the banking layer.

Can a Processor Legally Replace the Casino as Payee?

The Compliance Perspective

From a compliance standpoint, a processor may lawfully appear as the payee under several models:

- merchant-of-record structures;

- collection-agent frameworks;

- payment facilitation;

- technical settlement services.

However, problems emerge where:

- the player is not informed that the processor collects funds on behalf of a casino;

- the gambling purpose disappears from the payment record;

- the bank-facing transaction no longer identifies the gambling merchant.

In those situations, the structure creates elevated risks involving:

- AML monitoring;

- payment compliance;

- transparency obligations;

- consumer protection;

- gambling regulation.

Critical Questions Any Compliant Model Must Answer

A legitimate structure should clearly establish:

- Who is the actual gambling operator?

- Is the operator licensed in the player’s jurisdiction?

- Is the processor acting on behalf of that operator?

- Does the player understand whom they are paying?

- Does the bank receive the gambling context?

- Is there a transparent refund and complaint process?

- Is the gambling purpose preserved throughout the payment rail?

If those questions cannot be answered clearly, the architecture itself becomes a compliance concern.

Consumer Protection Concerns

EU consumer law requires transparency and material disclosure.

Consumers must understand:

- the identity of the trader;

- the nature of the service;

- who controls their funds;

- who handles disputes and refunds.

In gambling-origin payment flows, those elements become materially important.

Where the casino name disappears and a processor replaces it, players may no longer know:

- who operates the gambling platform;

- who ultimately receives the funds;

- whether the transfer is classified as gambling;

- where legal claims should be directed.

This does not automatically establish illegality in every case, but it creates significant misleading-omission and transparency risks — especially where the gambling operator lacks local authorisation.

AML and Payment-Compliance Risks

1. Payee vs. Ultimate Merchant

Banks, PSPs, PISPs, and MSBs must understand the true economic purpose behind transactions.

If entities such as CAPITOLIO INC. or Domus Payment Solutions appear as payees for casino-origin deposits, their role should be fully transparent:

- merchant of record;

- collection agent;

- settlement provider;

- processor;

- or technical intermediary.

2. Elevated AML/KYB Exposure

Gambling-origin payments are inherently high-risk because they may involve:

- money laundering typologies;

- fraud exposure;

- affordability concerns;

- consumer-harm risks;

- unauthorised gambling operations.

A processor receiving gambling-related funds should maintain KYB documentation covering:

- upstream casino operators;

- contractual relationships;

- licensing analysis;

- target jurisdictions;

- settlement flows;

- transaction-monitoring logic;

- complaint-handling procedures.

Without those controls, processor-as-payee structures may effectively become collection layers for unauthorised offshore gambling businesses.

3. Payment-Purpose Dilution

Scam-Or Project describes “payment-purpose dilution” as the process whereby a casino deposit appears downstream merely as a transfer to a processor.

This creates a dangerous visibility gap:

- banks see a processor;

- the economic reality is an offshore gambling transaction.

Impact on Player Refund Rights

No Chargeback Framework

For players, Pay-by-Bank structures create several disadvantages simultaneously:

- payments are harder to reverse;

- bank statements may not identify the casino;

- the gambling operator may be offshore;

- processors may deny merchant responsibility;

- banks may argue the transfer was authorised.

This significantly weakens the practical enforceability of player rights.

The Enforcement Problem

What Players Must Prove vs. What Payment Rails Show

| Player Must Prove | What the Payment Rail May Show |

|---|---|

| Deposit funded unauthorised gambling | Transfer to CAPITOLIO INC. or Domus Payment Solutions |

| Casino received the funds | Casino not visible as payee |

| Operator lacked local licence | Gambling merchant absent from records |

| Refund claim belongs against casino | Processor claims technical-only role |

| Bank should treat transaction as gambling | Bank sees ordinary A2A corporate transfer |

| Payment should be disputed | No card-scheme protections available |

This creates a direct conflict:

- the legal system may provide restitution rights;

- the payment architecture may obstruct their practical enforcement.

Compliance Risk Classification

| Risk Area | Assessment |

|---|---|

| Payment transparency | High risk |

| Consumer protection | High risk |

| AML/KYB exposure | High risk |

| Gambling compliance | High risk |

| Bank monitoring | Impaired visibility |

| Refund rights | Weaker than card rails |

| Litigation and restitution | Potentially obstructed |

| Regulatory reporting | Reduced upstream transparency |

Scam-Or Project Position

Processor-as-payee structures are not automatically unlawful. However, in offshore gambling payment flows, they represent a major compliance red flag.

A defensible model would require:

- transparent disclosure of the gambling operator;

- clear indication that processors act on behalf of the casino;

- preservation of payment-purpose visibility;

- documented KYB and onboarding procedures;

- jurisdictional licensing verification;

- blocking of prohibited jurisdictions;

- transparent refund procedures;

- transaction monitoring that preserves gambling context;

- auditable settlement trails.

Without those safeguards, the architecture risks becoming a practical concealment mechanism for the true merchant and payment purpose.

Questions for Processors, PISPs, and Banks

Scam-Or Project believes the following questions should be addressed whenever a processor appears as payee in gambling-origin open-banking rails:

- Who is the underlying gambling operator?

- Does the processor collect funds on behalf of that operator?

- Is the operator licensed locally?

- What merchant category and risk classification apply?

- What information does the payer’s bank actually receive?

- Does the PISP preserve upstream merchant context?

- Is the player informed about the processor relationship?

- Who handles refund and restitution claims?

- Can a complete audit trail be produced?

- Are unauthorised jurisdictions blocked?

If these answers remain unclear, the payment rail itself should be considered high-risk.

Conclusion

The processor-as-payee structures observed in 1Go Casino and Winnita highlight a serious weakness within modern open-banking gambling payments.

The player believes funds are being deposited into a casino account. The bank-facing layer may instead display a payment processor. Traditional card protections disappear. The operator may be offshore, opaque, or unlicensed locally.

At the same time, recent CJEU rulings confirm that Member States may attach restitution consequences to unauthorised gambling operations.

This creates the central conflict:

- players may legally possess refund rights;

- payment architecture may make those rights difficult to enforce.

For processors, banks, PISPs, and gambling regulators, the issue is no longer theoretical. Where entities such as CAPITOLIO INC. or Domus Payment Solutions appear as visible payees within casino-origin open-banking rails, transparency obligations become critical.

Open banking represents a major payment innovation. It should not become a mechanism for obscuring offshore gambling activity.

Scam-Or Project will continue documenting these payment rails because payment transparency has become central to consumer and player protection.

Call for Information

Scam-Or Project invites casino players, payment-industry insiders, compliance professionals, PSP employees, banking staff, and former gambling-sector employees to provide confidential information concerning processor-as-payee casino payment structures.

Relevant materials may include:

- bank screenshots;

- payment confirmations;

- open-banking consent screens;

- merchant descriptors;

- refund correspondence;

- PSP onboarding files;

- settlement records;

- internal compliance communications.

The investigation particularly concerns payment flows involving:

- CAPITOLIO INC.;

- Domus Payment Solutions;

- InstantBankPayment;

- Token GmbH/Token.io;

- Yapily;

- SaltEdge/Bridge;

- Revolut;

- related offshore casino payment rails.

Information may be submitted confidentially via Scam-Or Project Complaints.